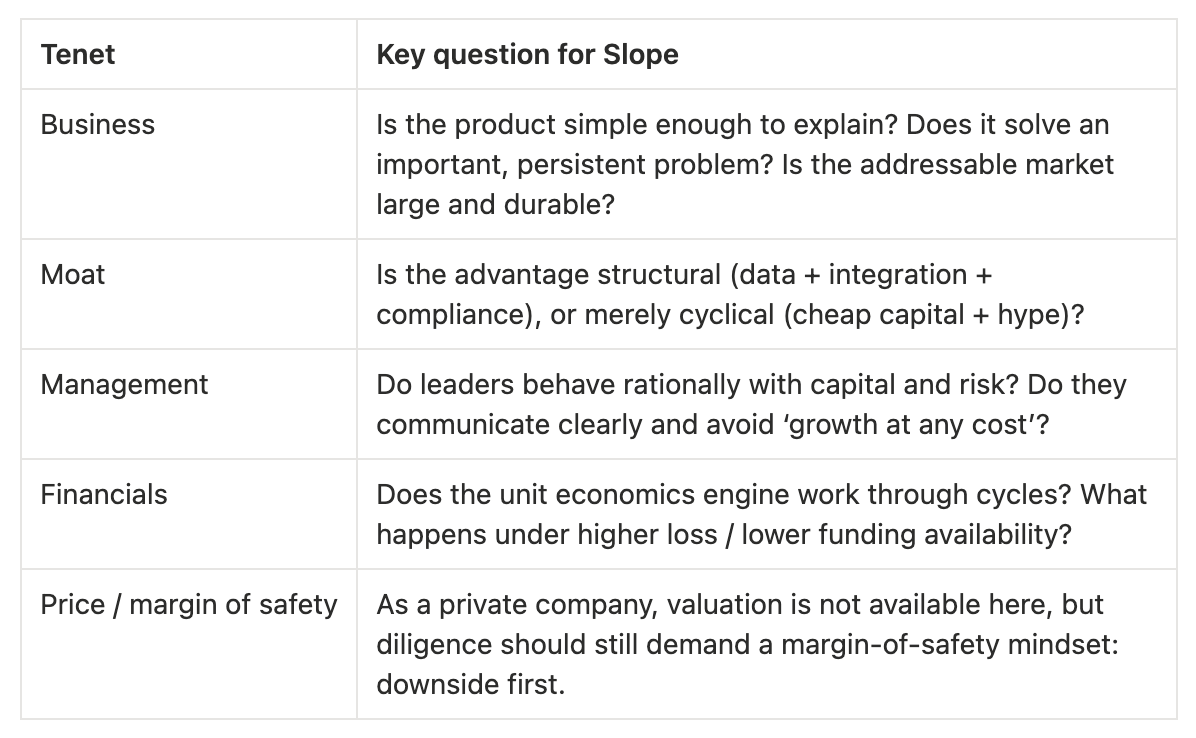

The Credit Layer You Don’t See

Inside Slope’s attempt to embed bank‑grade underwriting into B2B workflows.

Slope is a fintech infrastructure company sitting at the seam between payments and credit: it helps platforms and enterprises embed B2B payment flows and short-term working-capital products directly into checkout, billing, or seller portals. The company describes itself as “AI-powered credit and risk infrastructure” and positions its core competency as real-time underwriting from transaction and cash-flow data.

Two product lines capture the strategy:

Embedded Capital: financing/terms embedded at the point of purchase (e.g., Net 60/90), plus configurable credit-line and purchase-order financing use cases.

SlopeScore: a cash-flow underwriting score and transaction-intelligence layer marketed to lenders and platforms as an API-first decisioning system.

Slope is not a bank; credit products are originated by Lead Bank.

The business: where value is created

The cleanest mental model for Slope is a “credit layer” that can be bolted onto existing commercial workflows. Where consumer BNPL lives inside a checkout button, Slope aims to live inside the less glamorous but higher-volume plumbing: net terms, invoice payment, and working-capital cycles for businesses.

A typical embedded-terms flow looks like this:

A platform (marketplace, enterprise eCommerce, billing system) offers Net 60/90 or installments at checkout.

Slope ingests permissioned data (bank transactions and/or platform performance data) and produces an underwriting decision in seconds/minutes.

Credit is originated by a partner bank (Lead Bank) and funded via facilities / capital structure set up by Slope; the merchant receives funds while the buyer repays on agreed terms.

Slope’s software handles monitoring, credit line management, and reconciliation hooks (order-to-cash).

In the company’s own phrasing, “real-time underwriting” is the wedge: the decision is meant to be fast enough to sit inside a purchase flow and precise enough to satisfy bank-grade risk standards.

Slope’s revenue model is not fully disclosed, but the official materials imply two monetization streams:

Balance-sheet or facility-backed lending economics (interest income / fees) tied to credit line utilization and repayment.

Software / infrastructure fees for APIs that power underwriting, KYB/KYC, monitoring, and order-to-cash automation.

Slope’s business is not one business but a portfolio of closely related ones, and the durability question is whether the underwriting layer becomes a long-lived “habit” for platforms.

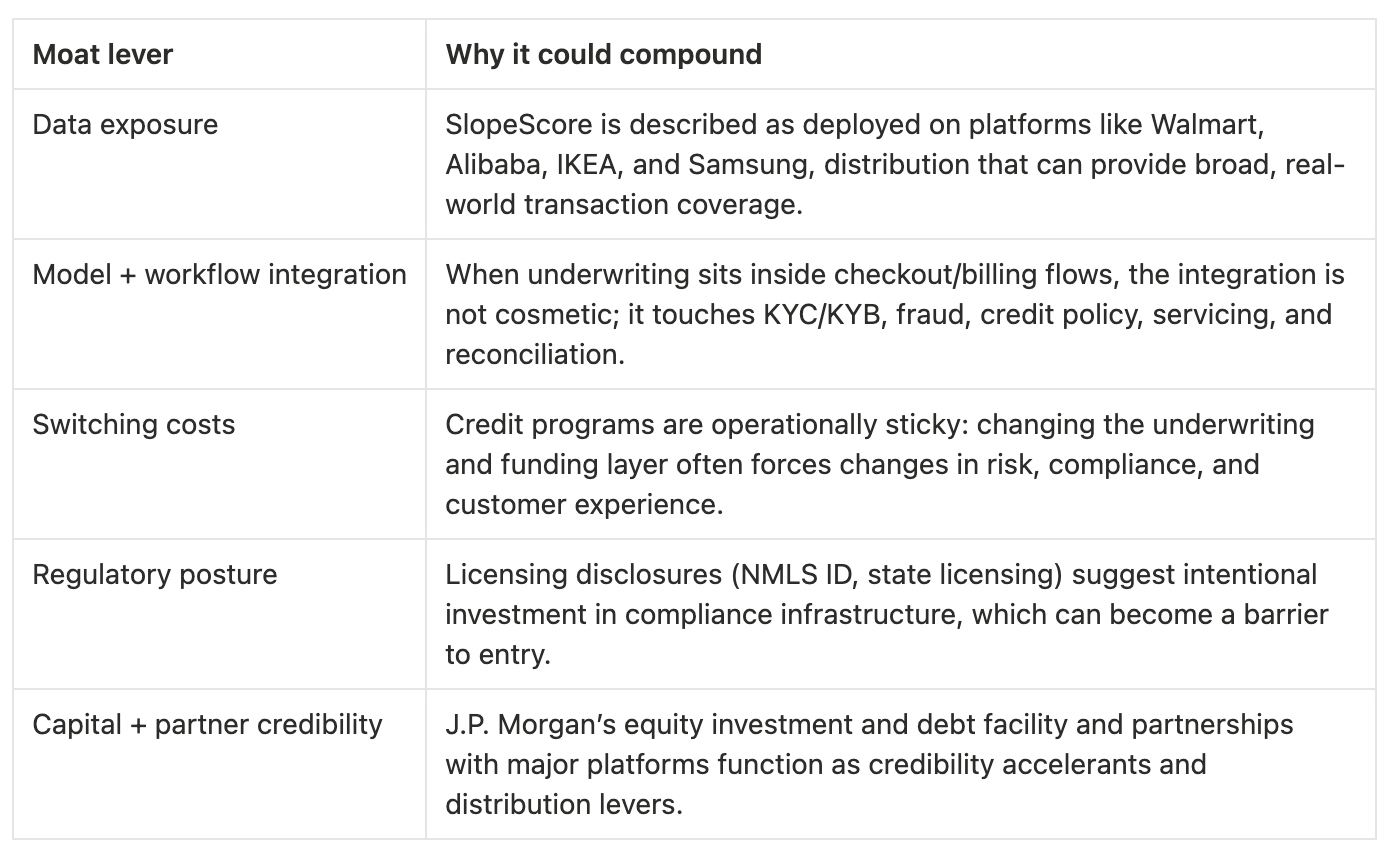

Moat, durability, and the data flywheel

Buffett’s default move is to ask whether a business has an enduring advantage that gets stronger with time. Slope makes the case that the advantage is the capital pool and transaction understanding: a specialized model that turns messy bank data into credit-grade signals at scale.

Management, culture, and incentives

Slope emphasizes their founder origin story and a simple mission: digitize B2B commerce and remove cash-flow friction. They frames the problem as the persistence of “offline, manual, and labor-intensive” order-to-cash processes.

Values that show up repeatedly are iteration speed and ownership.

The clearest observable evidence of operating tempo comes from employee accounts around major partner launches. In a December 2025 post about the Amazon lending rollout, Slope’s partnership lead wrote that the team “completed the integration in just 1.5 months” despite being lean.

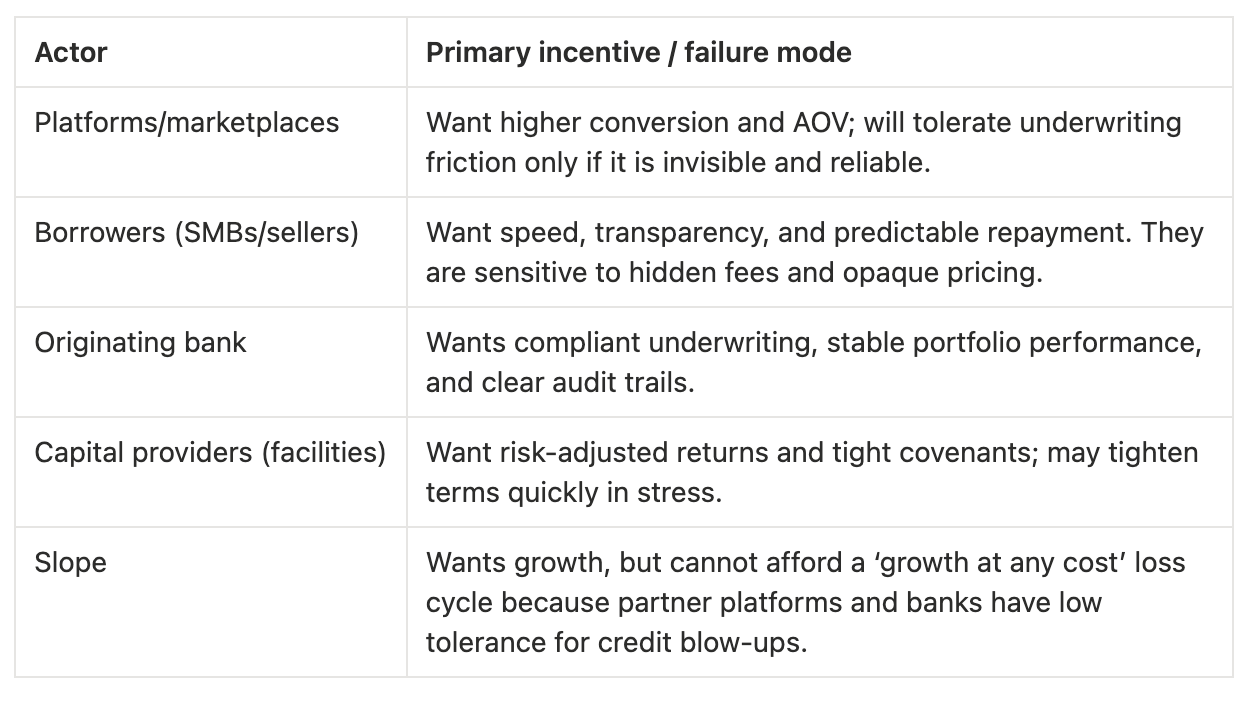

A useful way to evaluate Slope is to map incentives across the embedded-credit stack:

An additional (imperfect but informative) signal of engineering intensity: Slope reports that OpenAI recognized it for surpassing 10 billion tokens processed through the API, framing this as evidence of production-scale AI underwriting.

Capital structure and allocation

In a private company, capital structure is often the most “public” window into strategy. Slope’s July 2024 press release states total funding of $252M, split between $77M equity and $175M debt.

Debt’s dominance is rational if the intent is to scale lending capacity; it is also a reminder that Slope’s performance is tethered to capital markets and facility terms. The Elite partnership disclosure is explicit that J.P. Morgan provides a debt facility “in connection with this program” while not directly originating or servicing credit lines.

A capital-allocator checklist

For Slope, the highest-leverage allocation decisions are likely to be:

Where to sit on the risk curve (credit policy): approvals vs losses.

How to fund growth: more debt capacity vs more equity resiliency.

Whether to monetize as software (recurring fees) vs as lending spread (capital-intensive).

When to walk away from partner requests that demand suboptimal risk pricing.

Operating evidence: metrics, case studies, and what they imply

Slope’s public claims cluster into two buckets: (1) underwriting lift (approve more with controlled risk) and (2) workflow lift (higher conversion/AOV via embedded terms). Because the company is private, these should be treated as directional until validated in diligence; still, the specificity is useful.

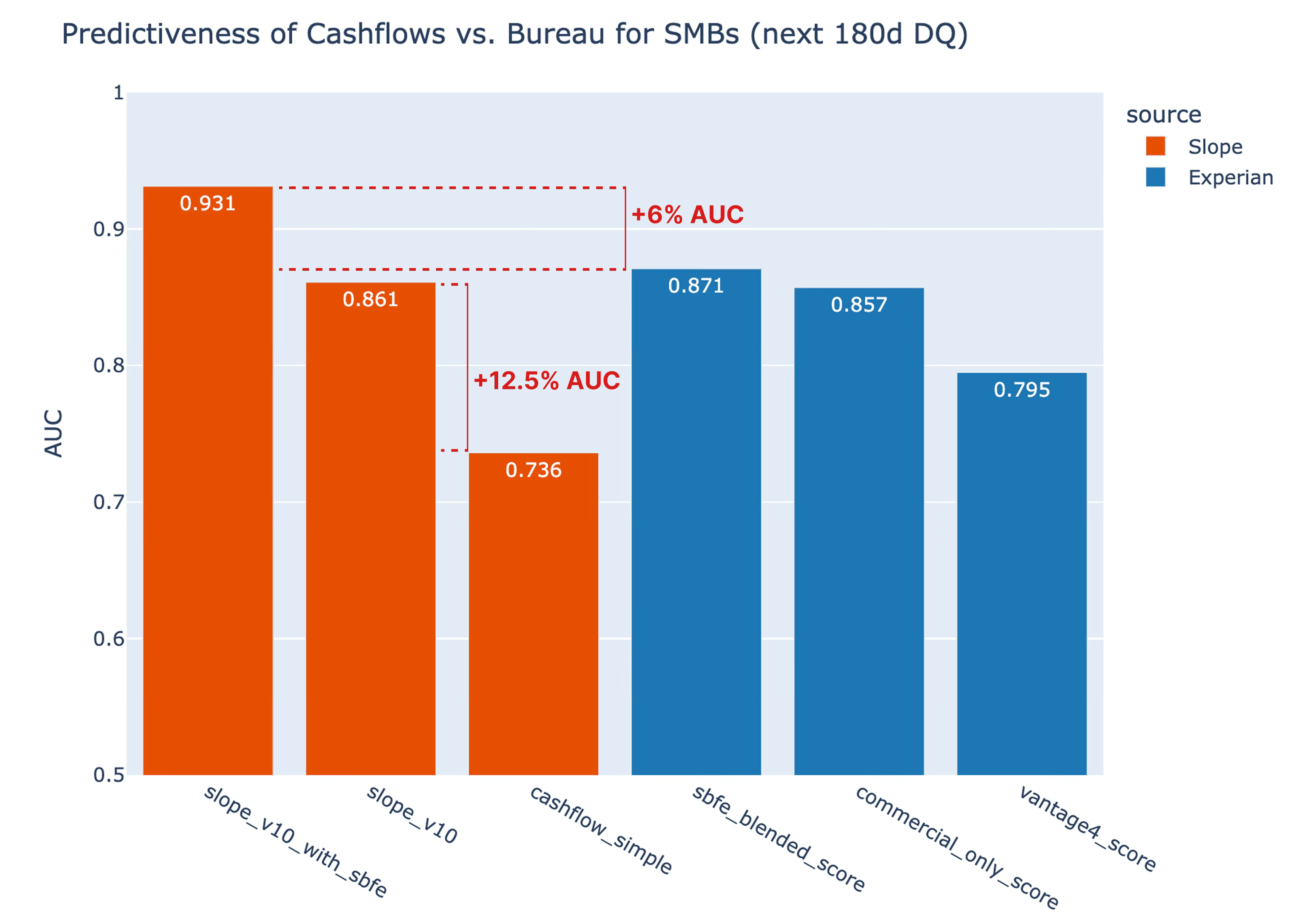

Underwriting performance (cash-flow scoring)

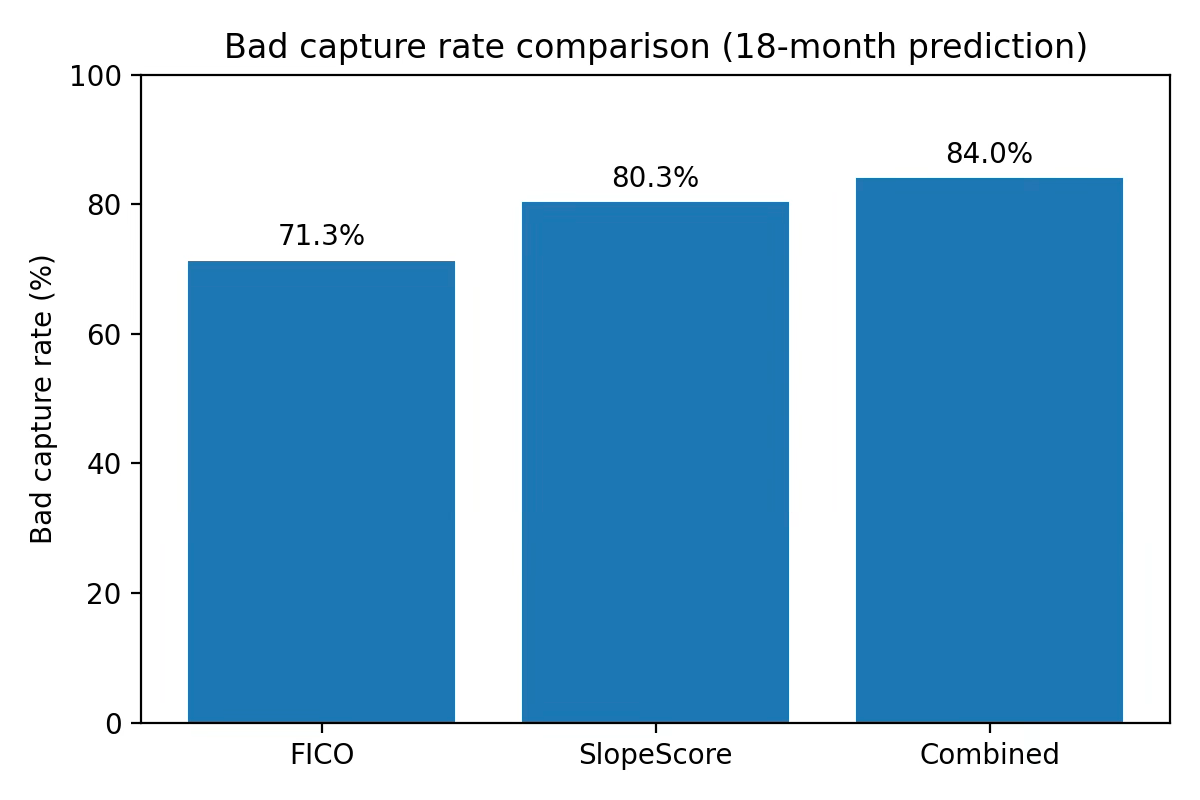

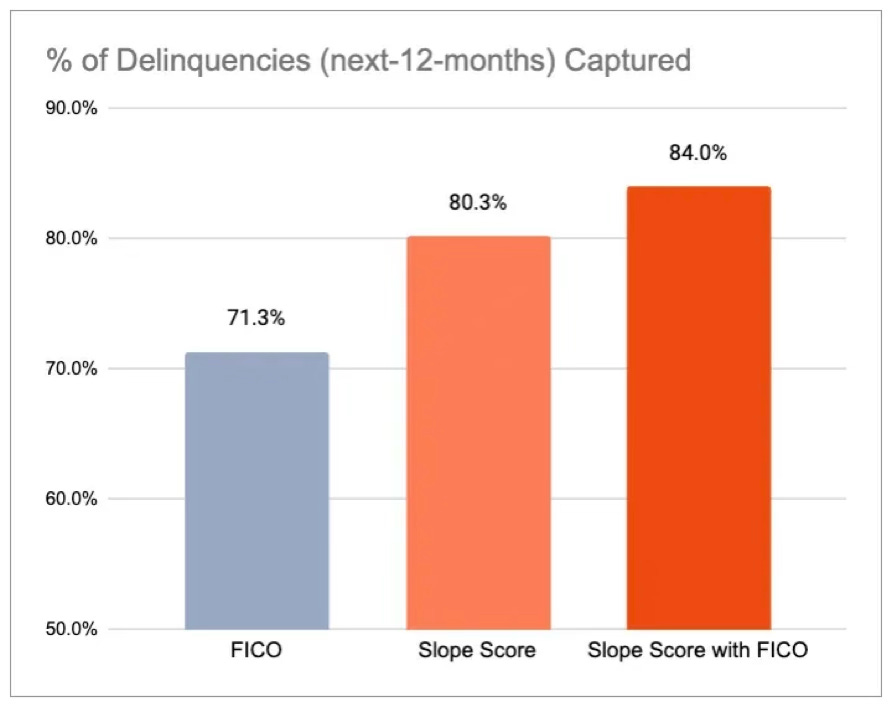

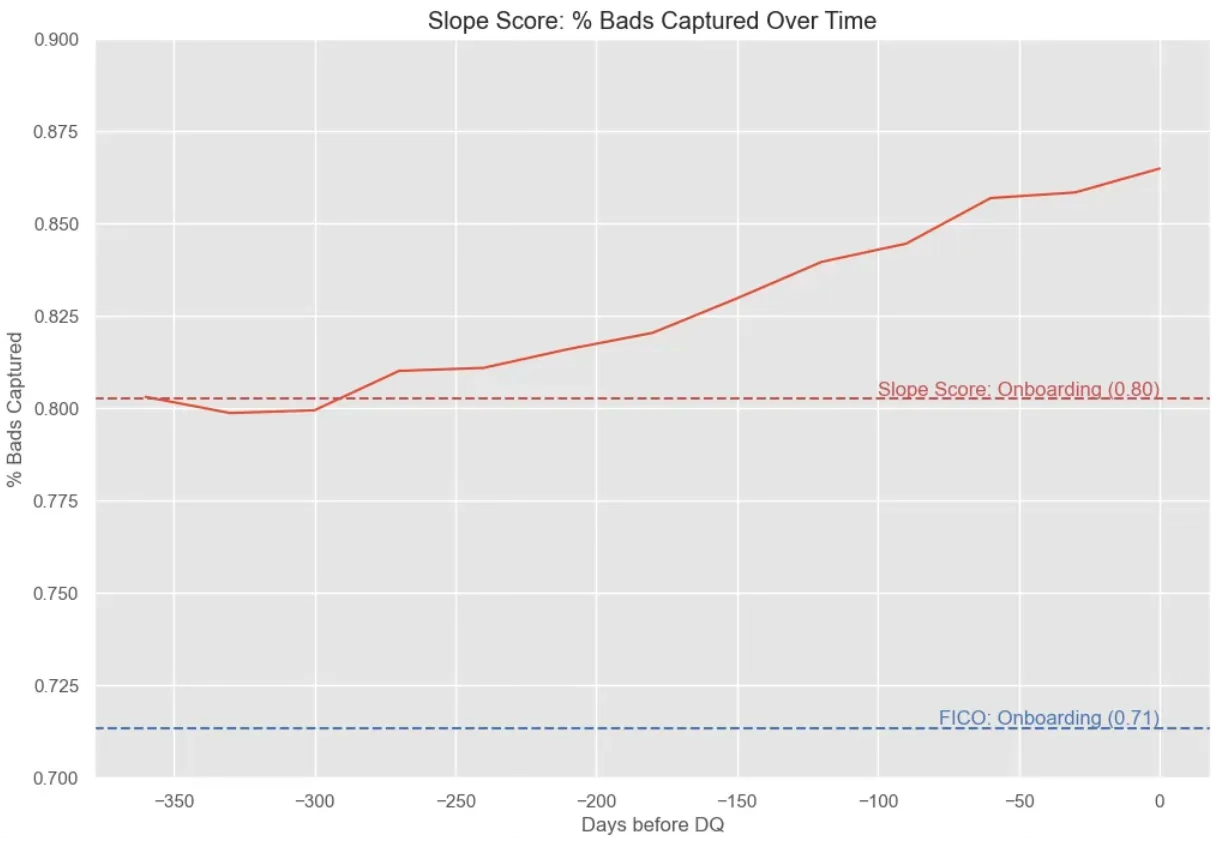

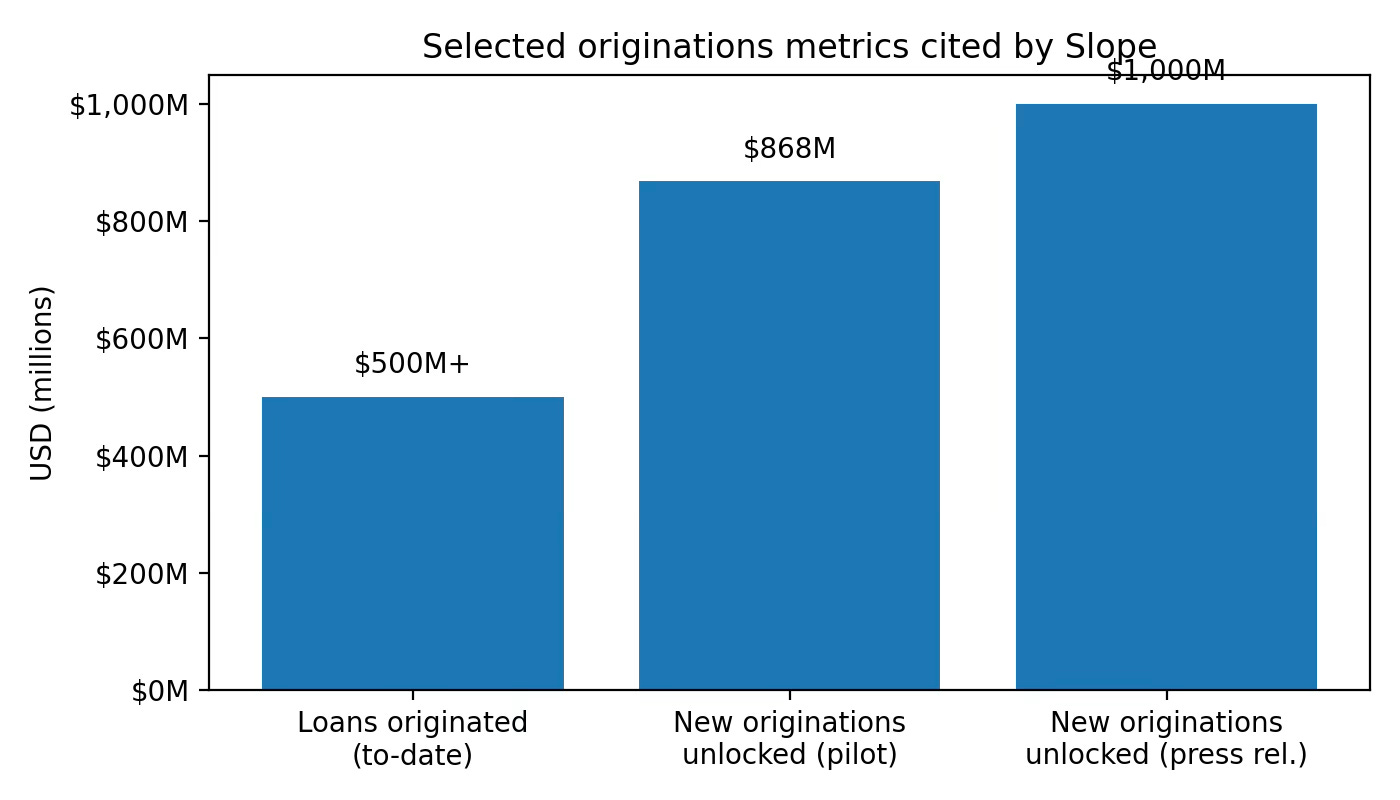

In a published case study with an anonymized “top U.S. bank,” Slope reports $868M in new profitable originations to near-prime and thin-file borrowers and a head-to-head bad capture improvement versus FICO.

Separately, Slope’s Business Wire launch release for SlopeScore claims that a pilot “unlocked nearly $1B in new credit originations,” delivered a lift over FICO, and achieved 99% transaction categorization accuracy in key fields.

Lending products and SMB outcomes (embedded credit)

Case studies focus on a practical thesis: credit terms are inventory strategy. In Slope’s Amazon-seller program description, the company advertises a reusable line of credit “up to $5M” for the strongest profiles, flexible terms, and an APR floor for top sellers.

In the GenCare case study, Slope describes an initial $250K line increased by another $100K, used to help fund a $400K product launch while the business maintained 100% year-over-year growth.

In another marketplace-focused case study, Kanso Worldshop pairs ~60-day supplier terms with Slope’s 90-day plan to create “roughly 150 days” of working-capital runway.

The Neato case study is the most explicit about margin mechanics: it describes using financing to pay suppliers upfront, capture discounts, and improve Amazon delivery speed, and reports a margin boost (bps) and an ROI multiple.

Scale signals (AI + originations)

Slope cites three scale signals: (a) $500M+ in SMB loan originations using its own capital, (b) automated approvals up to $250K based on bank data in some flows, and (c) 10B tokens processed via OpenAI’s API as a proxy for production AI usage.

Risk, regulation, and model governance

Credit businesses fail in boring ways: a few quarters of mispriced risk, a funding line that tightens at the wrong time, or a compliance process that breaks under scale. Slope acknowledges key parts of that reality through repeated bank-origination disclosures and a licensing page that enumerates state-level requirements.

Regulatory / structural dependencies

Bank dependency: credit products are originated by Lead Bank (Member FDIC). This creates a reliance on bank relationships, underwriting alignment, and program governance.

Funding dependency: debt facilities are a growth accelerant, but they are also a risk amplifier if covenants tighten or markets freeze.

Collections and servicing: licensing disclosures include collection-agency and money-broker licenses in multiple states; operational rigor here is not optional.

Model risk (especially for LLM-centric underwriting)

Slope markets SlopeScore as “FCRA compliant, explainable and customizable,” and highlights accuracy and fraud detection use cases. Those claims point to an implicit model-governance burden: explainability, stability under drift, and fairness / adverse-action workflows.

Slope emphasizes why SMB cash flow is hard: complexity, diversity, and context-dependence. This is simultaneously the company’s moat narrative and its principal technical risk.

Concentration and partner-risk

Slope’s growth narrative is partnership-led: Amazon seller lending, Samsung Business checkout terms, Alibaba.com checkout financing, and an Elite integration in legal billing. The upside is distribution. The downside is concentration: a single platform policy change can meaningfully alter unit economics and volume.

A useful inversion question: what would you do if you wanted to break this business? You would (a) pull a critical data feed, (b) tighten the facility, (c) trigger a compliance escalation, or (d) induce a cohort of correlated losses. These are the failure modes to diligence explicitly.

What must be true (checklist) + diligence questions

Given limited public financial disclosure, the most useful output is a checklist that connects Slope’s stated advantages to verifiable realities. This is the posture: don’t be impressed by cleverness; be impressed by what survives contact with incentives, time, and accounting.

Inversion and mental models

Zoom in on incentives, fragility, and human error under stress:

Incentives: are underwriting standards aligned between Slope, the originating bank, and distribution platforms?

Base rates: what is the historical loss rate by cohort and channel? How does it behave in downturns?

Second-order effects: does faster approval create adverse selection (good borrowers already have options; bad borrowers rush)?

Model risk: what is the monitoring/override process when the model drifts or behaves unexpectedly?

Capital allocation questions

How does Slope decide between expanding debt capacity versus strengthening equity buffers?

What return-on-capital thresholds govern partner program expansion?

Is growth constrained by underwriting confidence or by funding lines?

Diligence questions (actionable)

Portfolio performance: vintage curves (loss, delinquency, prepayment) by channel (Amazon, Samsung, etc.).

Unit economics: take rate / net interest margin, CAC (if applicable), servicing cost, expected loss, contribution margin.

Facility terms: key covenants, advance rates, triggers, and concentration limits.

Compliance: adverse-action process, audit trails, model documentation, and third-party risk management.

Data rights: what happens if Plaid, Amazon, or another key data feed changes terms or access?

Competitive resilience: which competitors can replicate the workflow (platform incumbents) versus the model (domain data)?

If Slope can answer these with clean data and conservative framing, the business begins to look like a compounding machine: integration-driven distribution feeding a data flywheel, producing better underwriting, producing more distribution. If it cannot, the same flywheel becomes a centrifuge.

Sources

Slope website (home) — https://www.slopepay.com/

Slope website (company/about) — https://www.slopepay.com/company

Slope product page: Embedded Capital — https://www.slopepay.com/products/embedded-capital

Slope product page: SlopeScore — https://www.slopepay.com/products/slopescore

Slope Tech licenses page — https://www.slopepay.com/licenses

Slope blog index — https://www.slopepay.com/blog

Slope case study: top U.S. bank SlopeScore pilot — https://www.slopepay.com/blog/top-us-bank-slopescore-case-study

Slope blog: SMB cash flow underwriting — https://www.slopepay.com/blog/state-of-business-cashflow-lending

Slope blog: OpenAI token award — https://www.slopepay.com/blog/slope-openai-token-award

Slope blog: Amazon press-release copy — https://www.slopepay.com/blog/slope-amazon-press-release

Slope blog: Amazon sellers line-of-credit program — https://www.slopepay.com/blog/slope-amazon-sellers

Slope case study: Neato — https://www.slopepay.com/case-studies/customer-neato

Slope case study: GenCare — https://www.slopepay.com/blog/gencare-case-study

Slope case study: Kanso Worldshop — https://www.slopepay.com/blog/walmart-kanso-worldshop-case-study

Slope blog: Alibaba partnership (press release copy) — https://www.slopepay.com/blog/alibaba-slope

Business Wire press release: funding round (Jul 17, 2024) — https://www.businesswire.com/news/home/20240717100691/en/Slope-AI-Led-B2B-Payments-Platform-Secures-%2465-Million-Strategic-Equity-and-Debt-Funding-Provided-by-J.P.-Morgan-and-Others

Business Wire press release: SlopeScore launch (Oct 7, 2025) — https://www.businesswire.com/news/home/20251007368878/en/Slope-Launches-SlopeScore-The-Cashflow-Score-for-Businesses

Business Wire press release: Samsung partnership (Nov 18, 2025) — https://www.businesswire.com/news/home/20251118180852/en/Slope-and-Samsung-Bring-Net-6090-to-Samsung-Business-Checkout-Powered-by-Real-Time-AI-Underwriting

Business Wire press release: Elite partnership (Oct 28, 2025) — https://www.businesswire.com/news/home/20251028413596/en/Elite-and-Slope-Partner-to-Provide-AI-Powered-Pay-Later-in-Legal

SEC Form D for Slope Tech, Inc. (filed Dec 2021) — https://www.sec.gov/Archives/edgar/data/1882129/000188212921000002/xslFormDX01/primary_doc.xml

LinkedIn post by Slope employee Keyi (Sophie) Wang (Dec 2025) — https://www.linkedin.com/posts/keyi-sophie-wang_im-thrilled-to-share-that-slope-has-officially-activity-7406746427407695872-kHMr

LinkedIn post by Slope (Samsung partnership) — https://www.linkedin.com/posts/slope-tech_were-excited-to-announce-our-partnership-activity-7396597739624701952-cKRb

LinkedIn post by Lawrence Lin Murata (Apr 2025) — https://www.linkedin.com/posts/lawrencelm_the-fastest-way-to-grow-originations-and-activity-7321218869044346882-q7Wh

Interesting view on embedding credit directly into workflows. As trade credit becomes more dynamic, the balance between speed and sound underwriting becomes critical. Integrating decisioning into O2C processes has clear potential - but maintaining visibility and control over risk will remain just as important.