Sierra’s Quiet Land Grab in Customer Experience

From support tickets to revenue workflows: what happens when CX becomes autonomous.

Sierra builds AI agents that let large companies deliver faster, more human customer service, at measurable scale.

Support Is a System Problem Masquerading as Headcount

Customer support leaders are stuck in a cursed triangle: customers want instant answers, companies want lower costs, and humans have finite time, patience, and consistency. The result: long queues, transfers, repetitive identity checks, and the ‘please restate your problem’ ritual that makes people feel like they’re talking to a goldfish.

How is this addressed today and what breaks:

Human agents + contact center software: works, but expensive and hard to scale; quality varies by training and turnover.

Static self‑service (FAQs, help centers): cheap, but brittle; it fails when the question is even slightly weird.

Rule-based chatbots / IVR trees: deterministic, but frustrating; they are good at ‘press 1’ and bad at ‘I have a complicated life.’

DIY ‘LLM wrapper’ bots: fast to prototype, hard to trust; hallucinations and policy drift become a production incident.

Outsourcing (BPO): trades cost for control; you still own the customer experience and the brand damage if it goes sideways.

Building a production-grade agent means you need policy enforcement, integrations into real systems, and a way to test the agent before customers do.

An Agent That Can Talk, Remember, and Act (Safely)

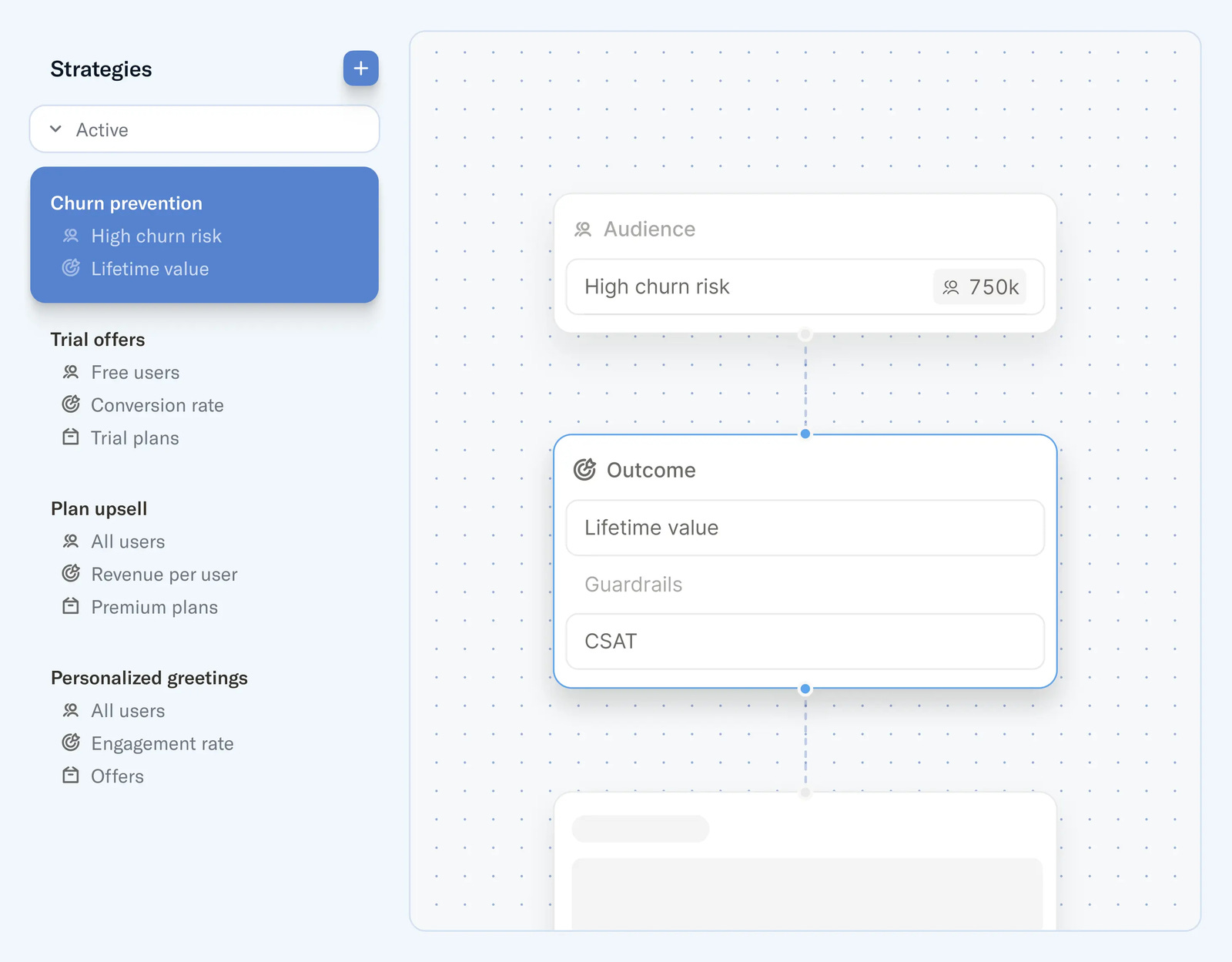

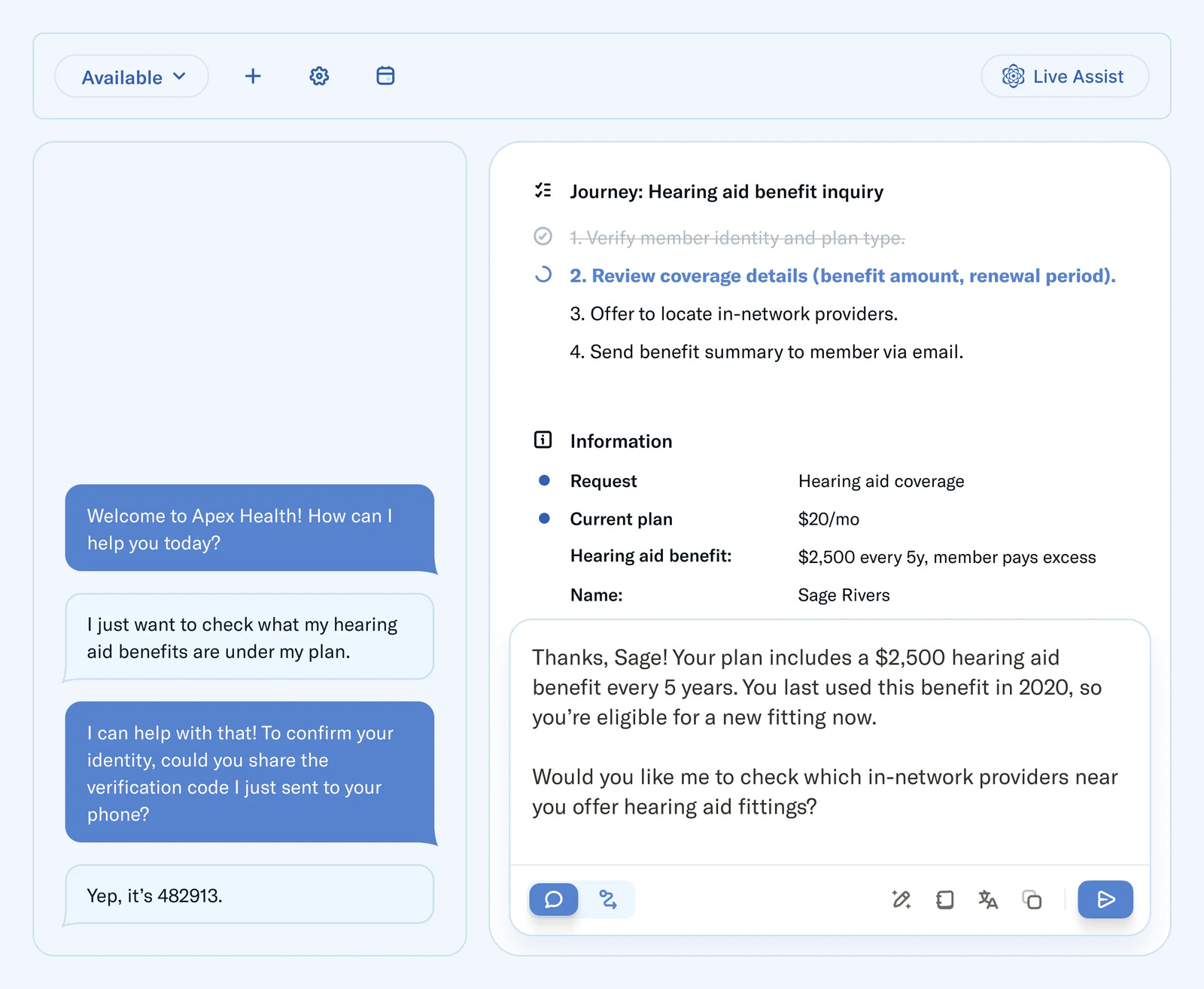

Treating an ‘agent’ as an operating system problem: conversation is the interface, but reliability comes from the plumbing: integrations, memory, supervision, testing, and monitoring, wrapped into a platform.

Sierra’s value proposition:

Enterprise-grade trust & reliability: multi-model orchestration, supervisor models, encryption, and governance posture to support regulated deployments.

Outcome orientation: the product and pricing story is ‘pay for results’ rather than ‘pay for seats.’

A single agent across channels: consistent experience across voice + digital rather than fragmented bots.

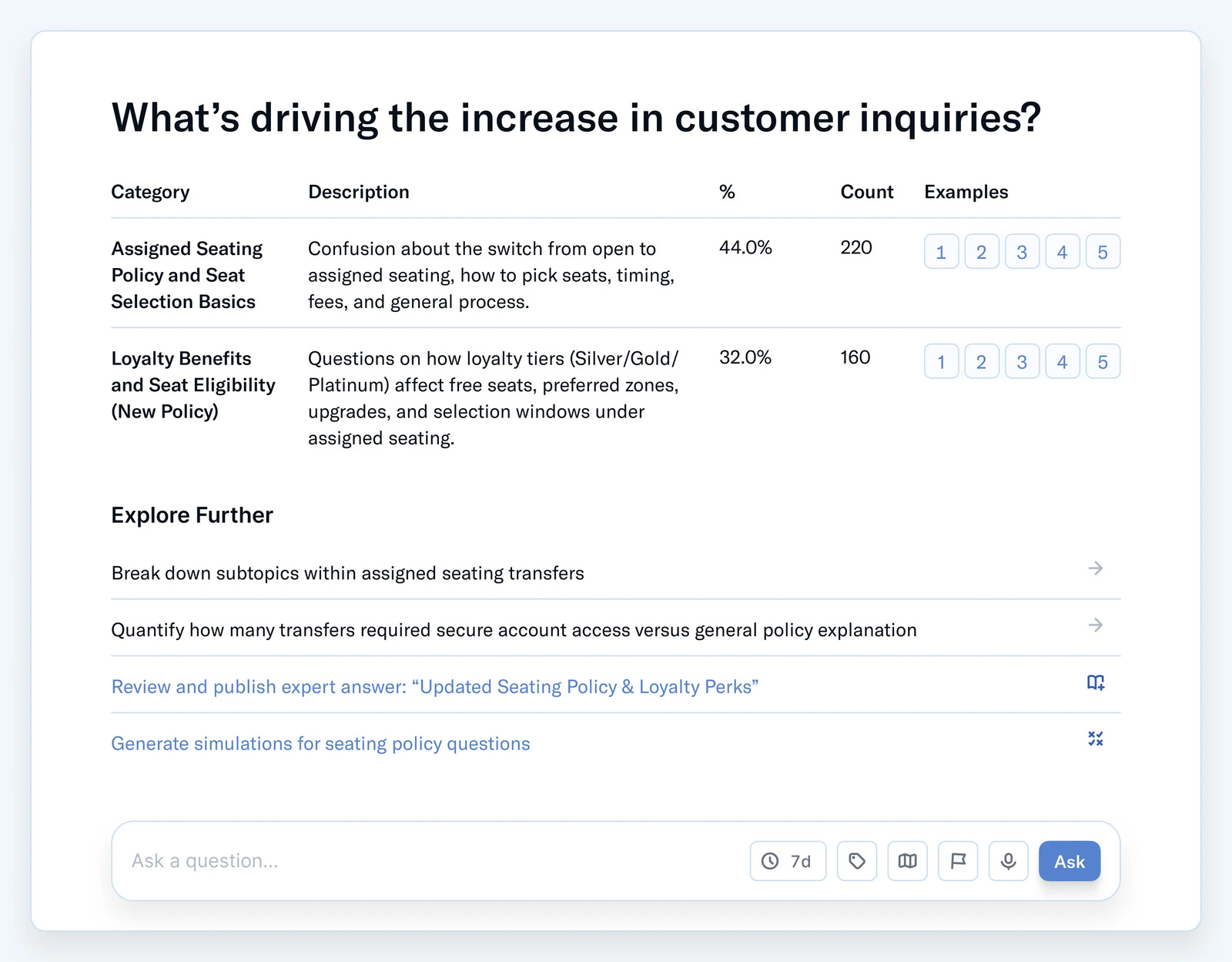

Measurement loop: simulations, benchmarks, and analytics turn agent quality into something you can iterate on like software.

Sierra’s endurance:

Switching costs: once the agent is wired into billing, identity, shipping, returns, and policy workflows, ripping it out is painful.

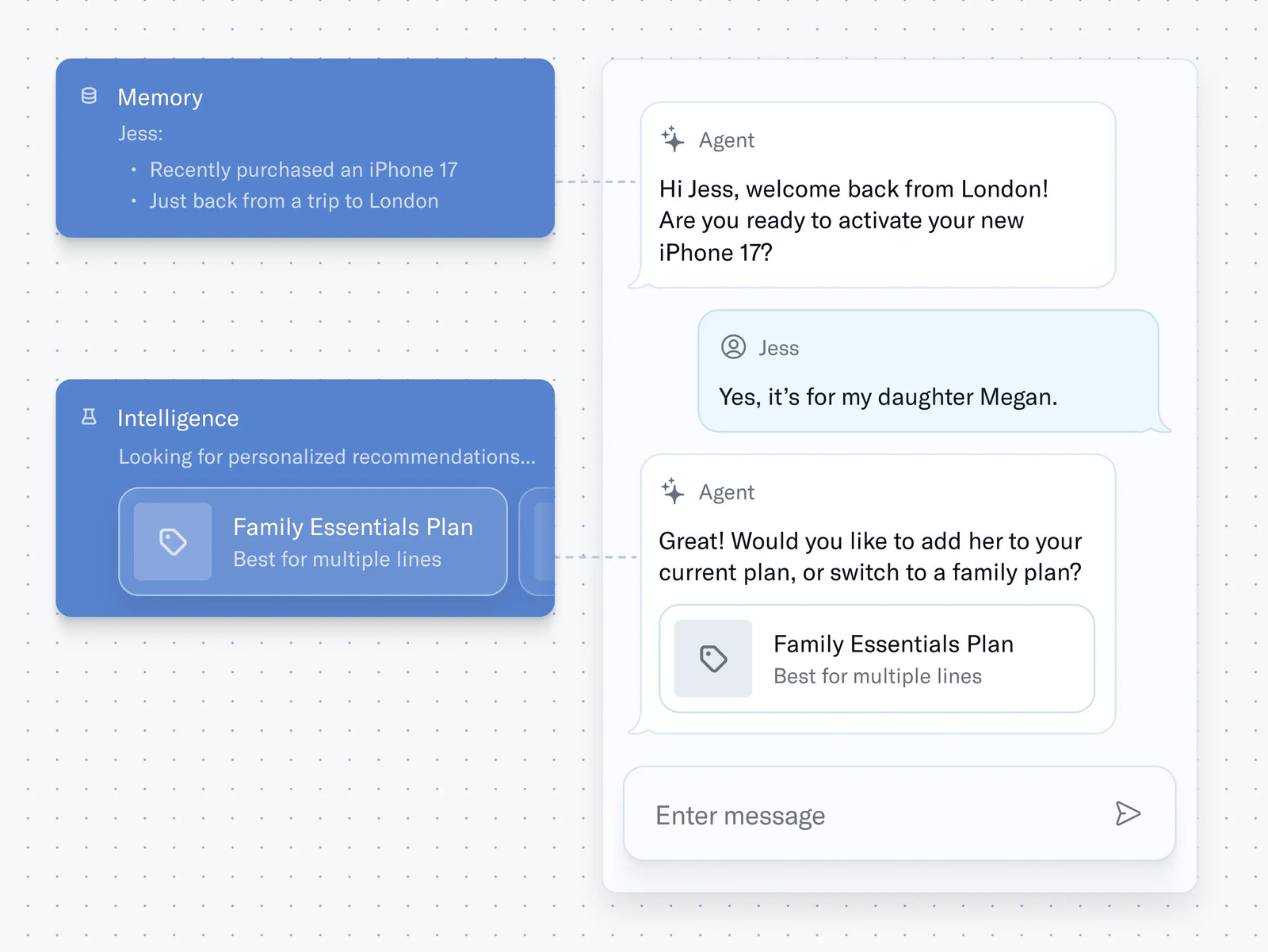

Data flywheel: the Agent Data Platform framing suggests Sierra wants to own customer context and the feedback loop from every interaction.

Operational know-how: reliability is a culture + toolchain that compounds over time.

Brand trust: in customer service, a single bad interaction can become a screenshot that does brand damage.

Sierra is then moving from ‘conversations’ to ‘relationships’: memory, personalization, proactive actions, and expansion beyond support into revenue workflows (retention, upsell, sales).

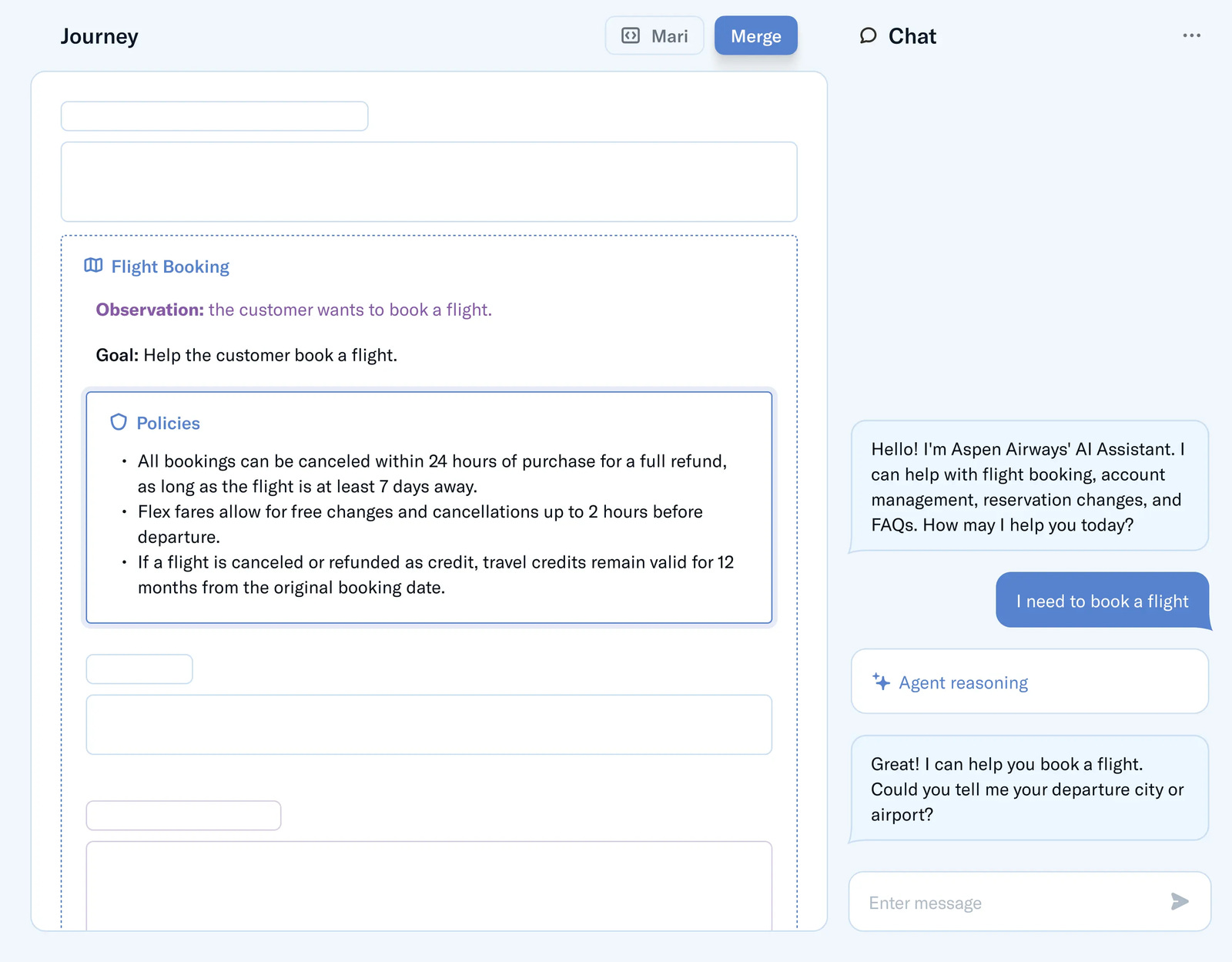

Architecturally, Sierra sits between customer channels (chat, email, voice, web, and now third‑party AI surfaces) and systems of record (CRM, billing, shipping, identity, knowledge base). It’s an orchestration layer: interpret intent → decide policy‑compliant action → execute via integrations → respond.

Use cases:

Customer support: refunds, order status, troubleshooting, account access, subscription changes.

Customer retention: proactive outreach, win-back flows, identifying at-risk customers.

Sales assistance (adjacent): product selection, plan changes, upgrades, especially where context matters.

Agent assist: copilots that help human agents resolve faster and more consistently.

Models Got Good Enough, and the Rest of the Stack Finally Caught Up

In the 2010s, automation in customer service mostly meant decision trees. In the early 2020s, large language models made natural conversation cheap, but not necessarily safe. The current moment (2024–2026) is when models, tooling, and enterprise governance have matured enough that you can plausibly ship agents that are both helpful and controlled, and you can justify them with ROI rather than vibes.

Why hasn’t the solution been built before now?

Pre‑LLM NLP was brittle: earlier chatbots required strict intent classification and collapsed under messy real‑world language.

Model costs and latency used to be prohibitive for high-volume customer service.

Tooling was immature: agents need evaluation, simulation, monitoring, and governance, capabilities that are now productized.

Enterprise readiness: compliance regimes (SOC 2, HIPAA, ISO, etc.) and procurement patterns are non-negotiable for big customers.

The historical evolution of the category:

Call centers → IVR trees → web chat → omnichannel contact center platforms.

Rule-based bots and knowledge bases tried (and mostly failed) to absorb volume.

LLMs unlocked natural language; the new frontier is making them reliable, integrated, and measurable enough for enterprises.

There is a convergence of better foundation models, better control patterns (supervision + guardrails), and a market shift from pilots to production where buyers demand proofs and paybacks.

The CX Stack Is Huge, and “Agentic” Expands the Boundary

Sierra is aimed at high-volume customer service operations in large enterprises, companies where a one‑point change in containment or CSAT can move real dollars. The company’s disclosed customer base spans fintech, media, consumer brands, e‑commerce, and more, basically: ‘lots of interactions’ businesses.

Categories are economic weapons, they create pricing power and reduce feature-by-feature comparisons. Sierra is attempting to reframe ‘customer service software’ into a newer category: AI agents as a primary interface for customer relationships.

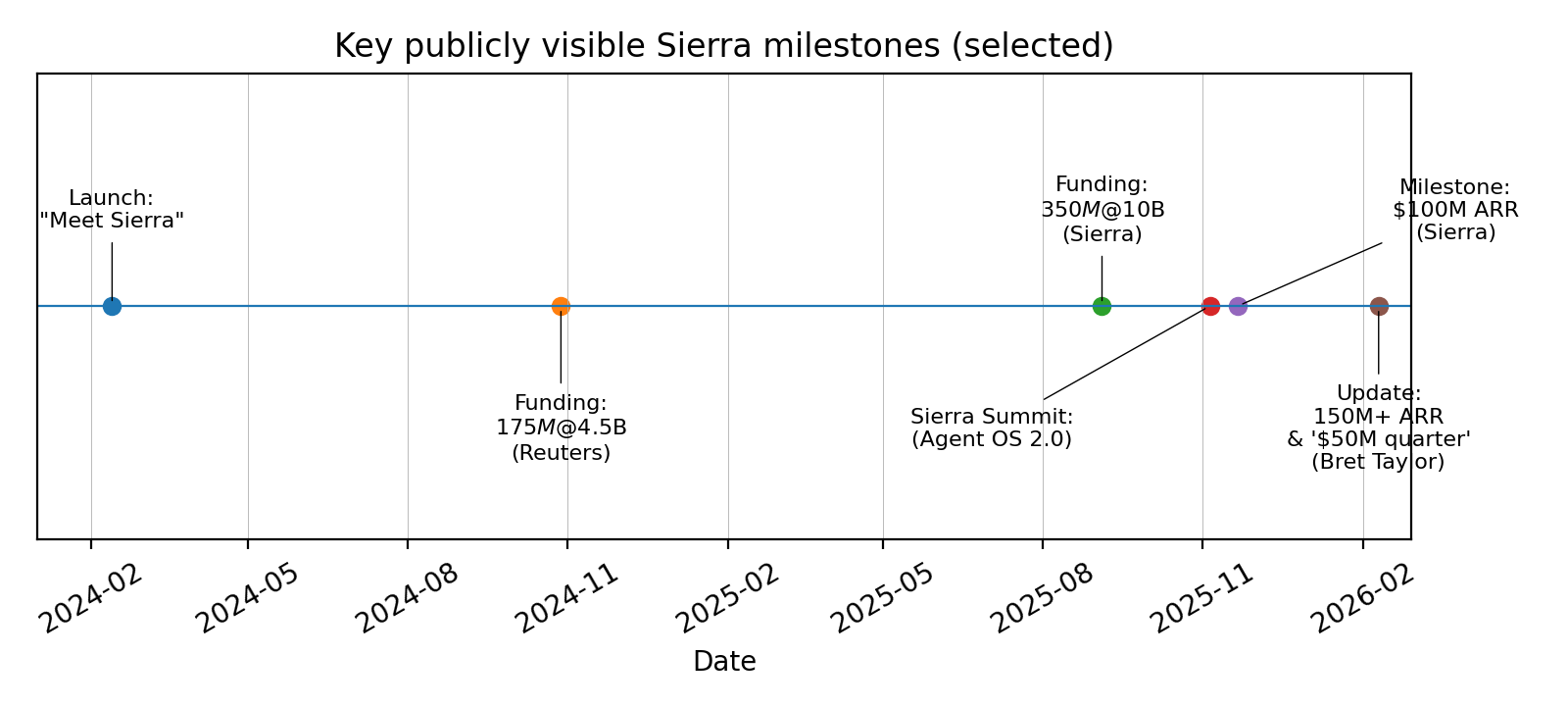

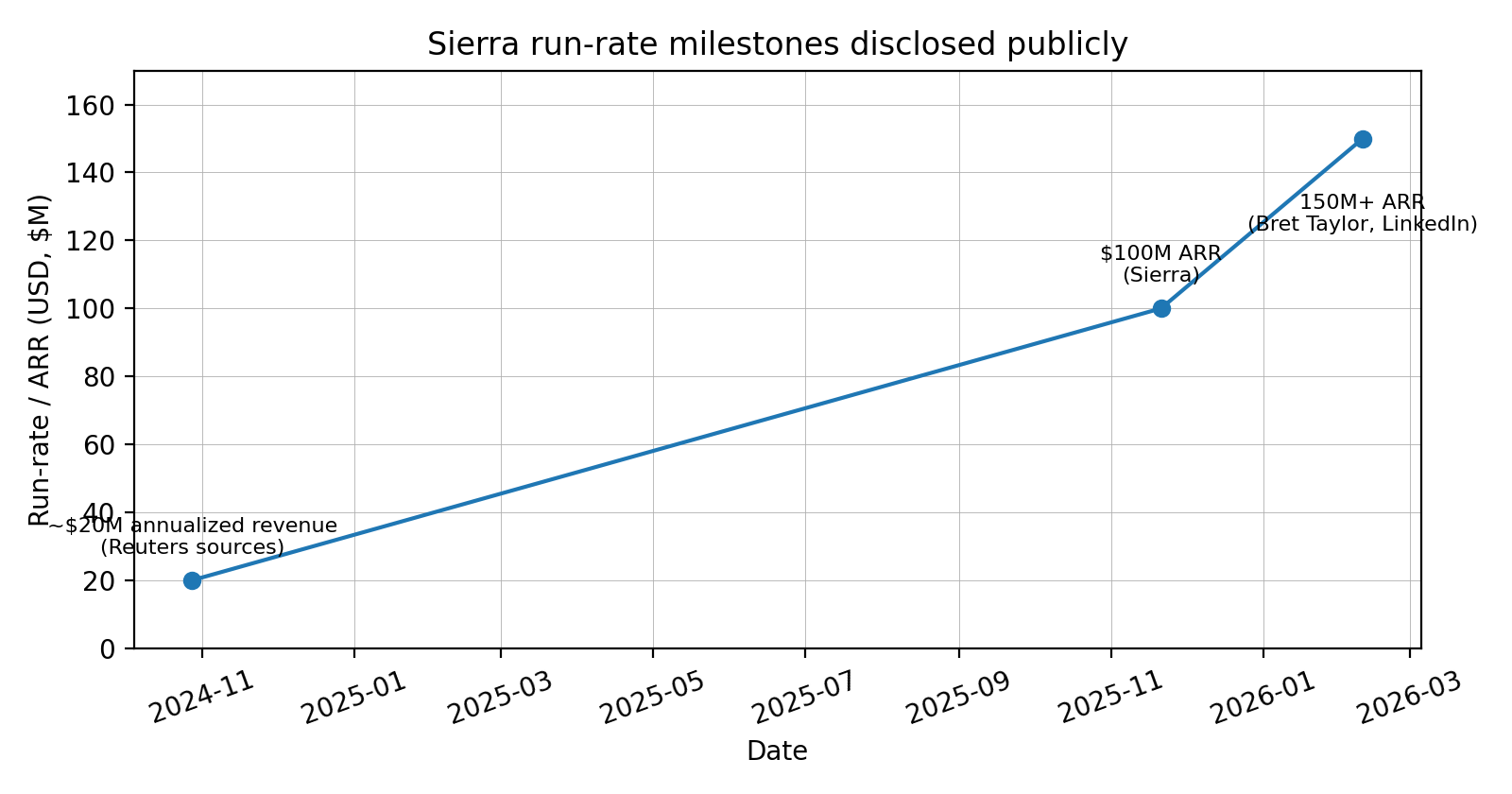

Sierra announced $100M ARR seven quarters after its February 2024 launch, then started 2026 with 150M+ ARR. Its customers as skewing large: more than half have >$1B revenue, and close to a third are in the Fortune 500.

Sample scaled deployments incude ADT (2M+ inquiries/month) and SiriusXM (34M+ subscribers), other disclosed logos include SoFi, Sonos, WeightWatchers, ScottsMiracle-Gro, Wayfair, Chime, and more.

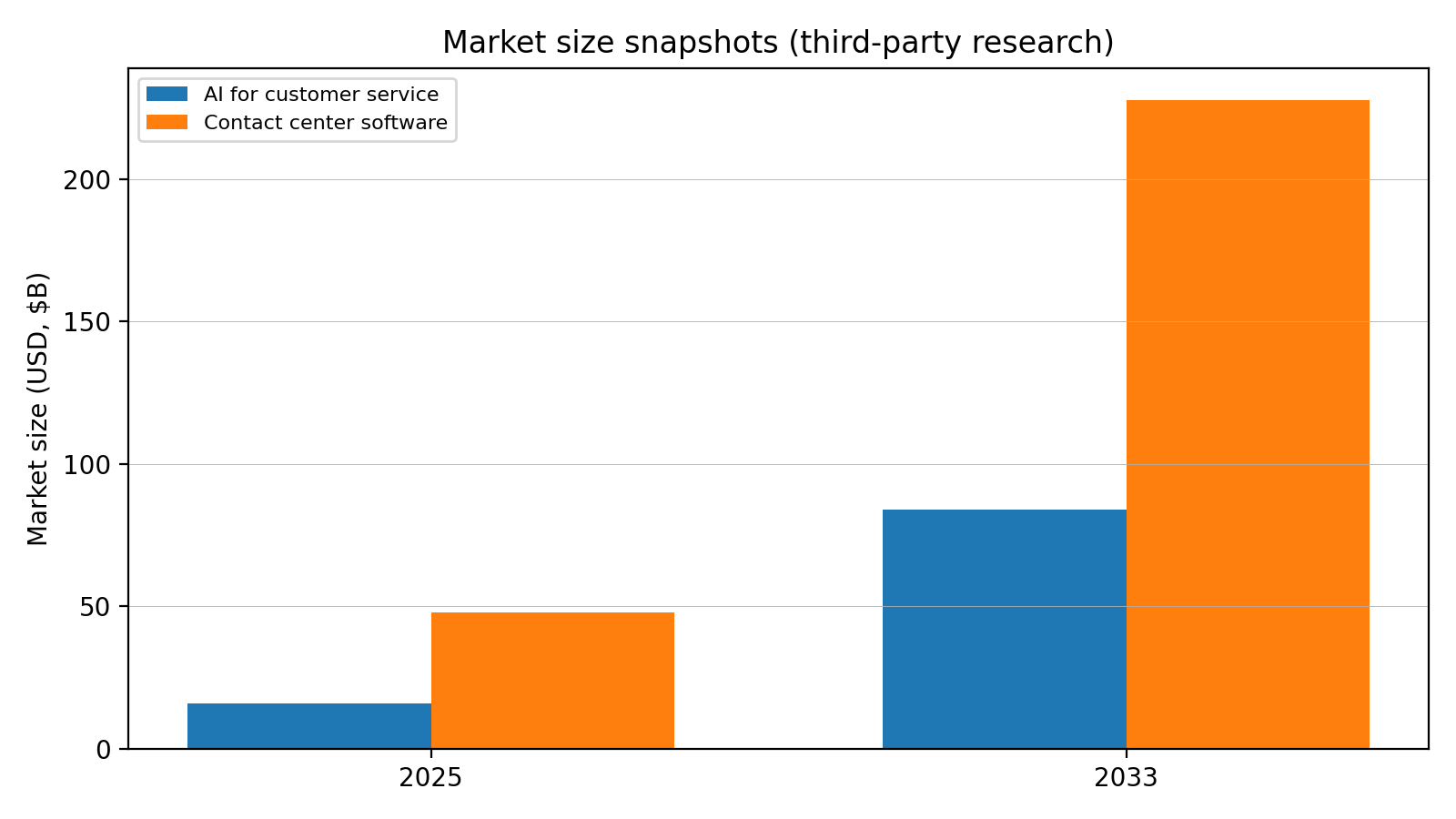

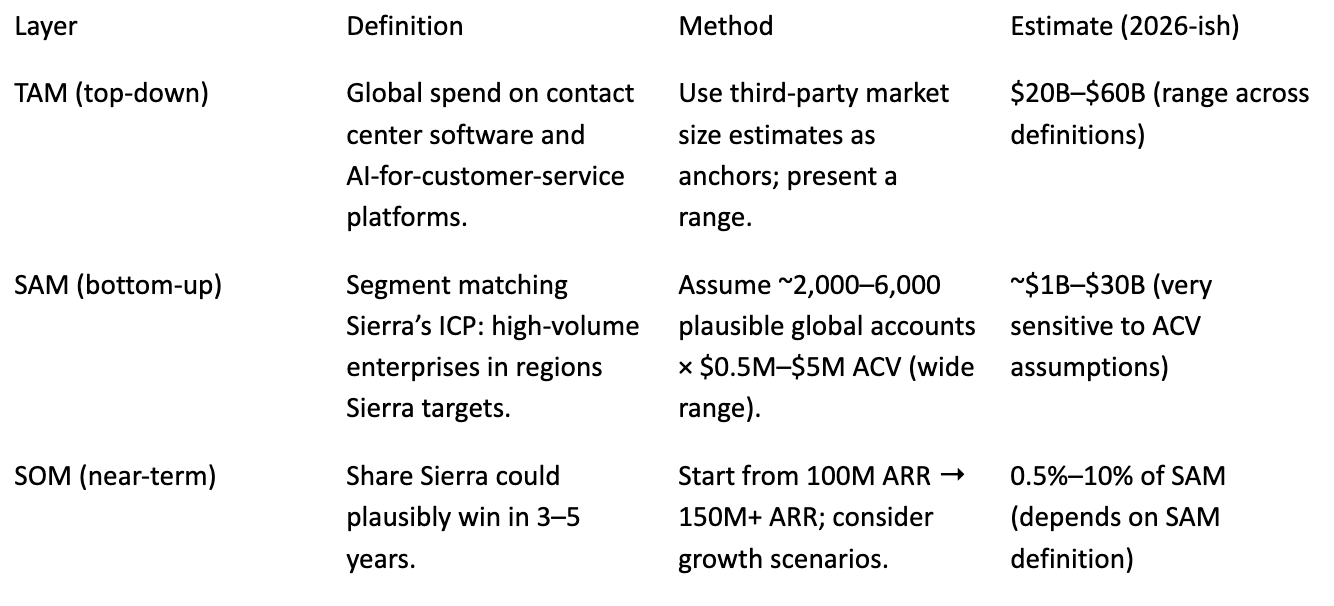

We provide two TAM anchors from third-party research: (a) contact center software spend and (b) AI for customer service spend.

Market sizing (USD), a structured estimate:

Everyone Has a Bot. Few Have a Platform

Who are Sierra’s direct and indirect competitors?

Direct: AI agent platforms and ‘AI first’ CX vendors (agent builders focused on support automation).

Adjacent incumbents: contact center and CRM suites layering AI into existing products (e.g., Salesforce, Zendesk, ServiceNow, NICE, Genesys, Five9).

In-house builds: teams that try to assemble an agent from an LLM + retrieval + a few API calls.

Non-software alternatives: BPO outsourcing and incremental process improvements.

Sierra’s implied plan to win is less about being the smartest model and more about being the safest system: trust, reliability, governance, and end-to-end integration. In enterprise buying, ‘cool’ is optional; ‘won’t blow up in production’ is mandatory.

Sierra’s competitive advantages:

Full-stack product: Agent OS + building tools + analytics + agent-assist, not a single point feature.

Reliability toolchain: supervision, simulations/benchmarks, monitors, and governance.

Outcome-based pricing reduces shelfware risk and signals confidence.

Founder credibility and network: leadership with deep platform-building experience; easier access to large customers and partners.

Large-deployment proof points: case studies emphasize scale and regulated environments.

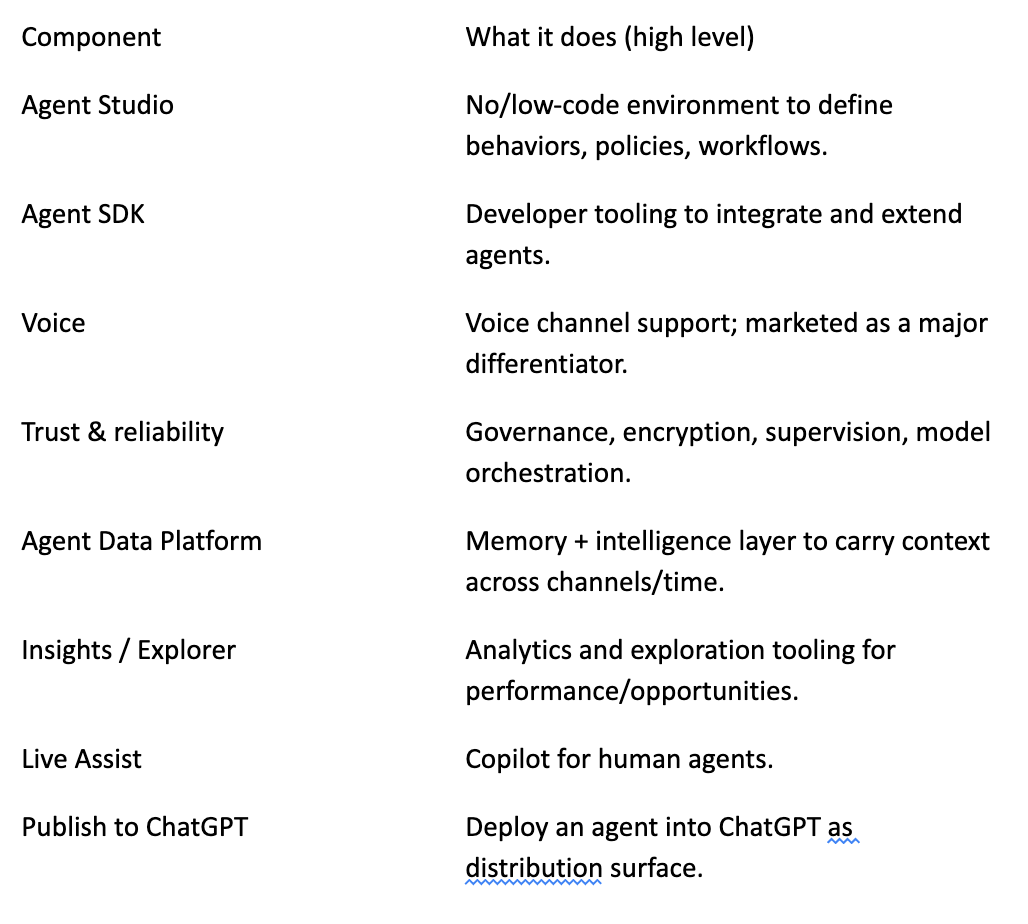

Product: Agent OS, Studio, and the Data Brain

Sierra’s product surface looks like an agent stack: build (Studio/SDK), deploy (multi-channel), supervise (trust layer), and learn (data + insights).

Outcome Pricing + Enterprise Motion

The company intends to thrive by doing the following:

Align incentives: emphasize outcomes and measurable impact, not seats and vanity usage.

Land-and-expand: start in a high-volume support domain, then expand to more workflows, more channels, and more business units.

Make reliability productized: testing, monitoring, and governance as repeatable software, not bespoke consulting.

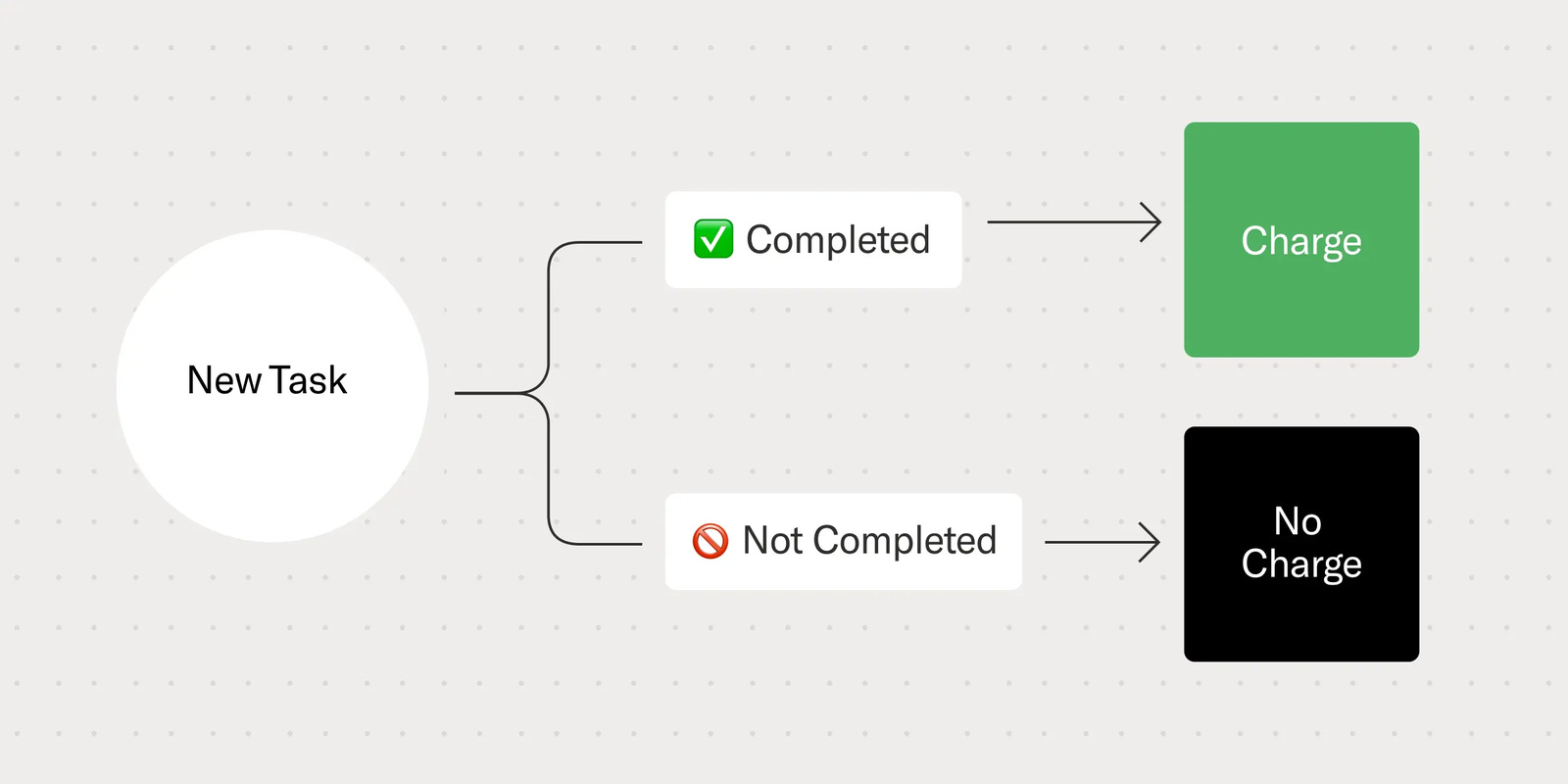

Sierra’s revenue model describes an outcome-based pricing model, charging when the agent completes a defined task successfully, rather than selling seats designed for human agents.

Pricing is framed around completed tasks/outcomes. What’s not public: per-outcome rates, minimums, and contract structures (likely vary by customer, channel, and complexity).

Sierra does not disclose ACV or LTV. The combination of 150M+ ARR and a customer base skewing to very large enterprises implies meaningful enterprise account sizes for scaled deployments.

Sales & distribution model:

Enterprise direct sales (implied by customer profile and procurement requirements).

Founder-led credibility early; the founding team has strong enterprise networks.

Platform distribution experiments: publishing agents into ChatGPT as a new top-of-funnel channel.

International expansion signal: Japan expansion with Softbank Vision Fund 2 support.

Sierra publicly lists customer stories and logos across industries (security, media, fintech, consumer brands, e‑commerce).

People Who’ve Built Platforms, and Know the Cost of Failure

Customer experience is a high-stakes, brand-sensitive domain. Execution matters. Sierra’s founders have prior experience building platforms at massive scale.

Bret Taylor, CEO and co-founder (previously Salesforce co‑CEO; earlier roles at Google; chaired Twitter’s board pre-acquisition).

Clay Bavor, co-founder (previously led Google Labs).

Rachel Whetstone, communications leader (joined from Netflix; previously at Uber and Google).

Investors (public):

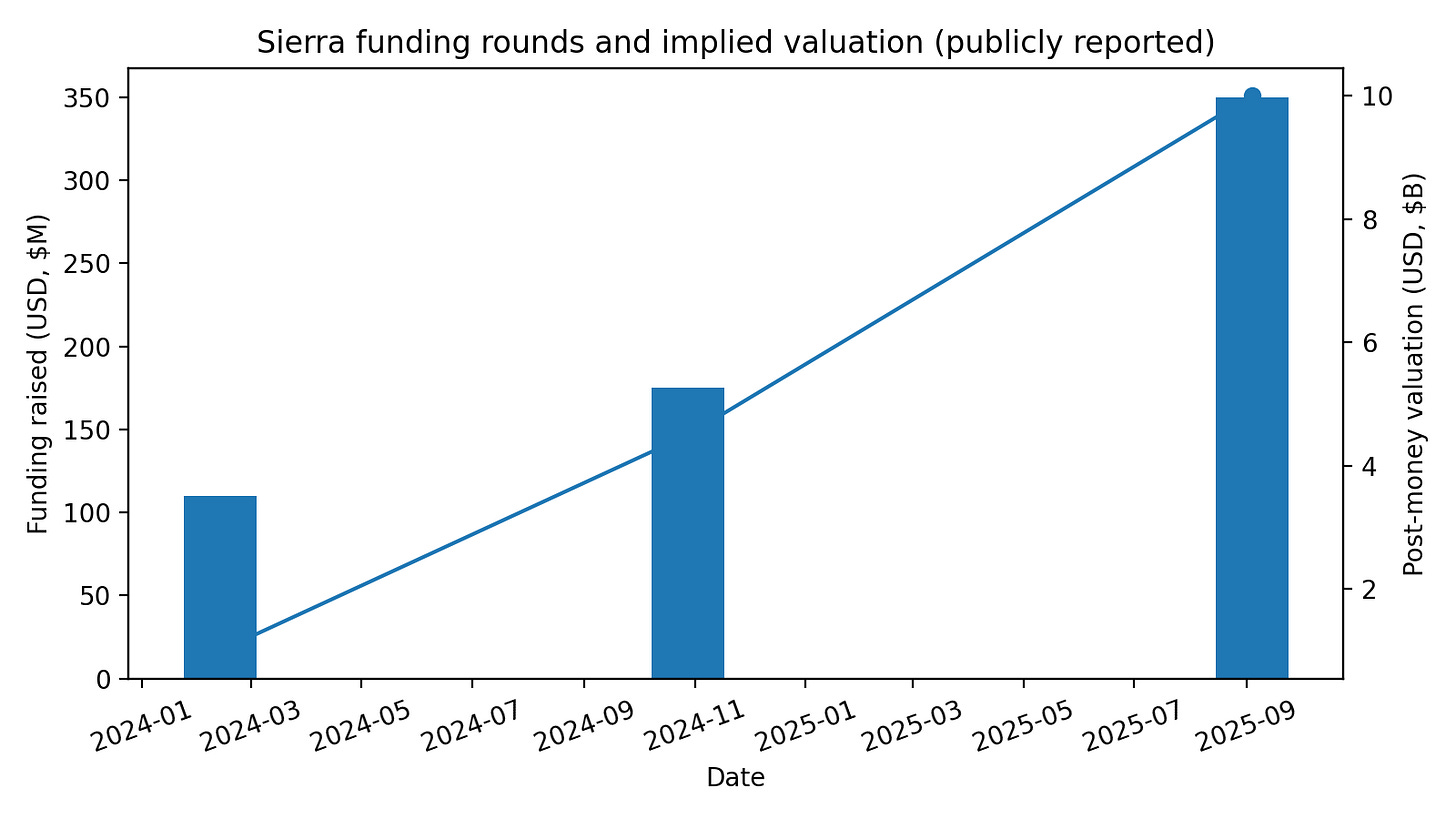

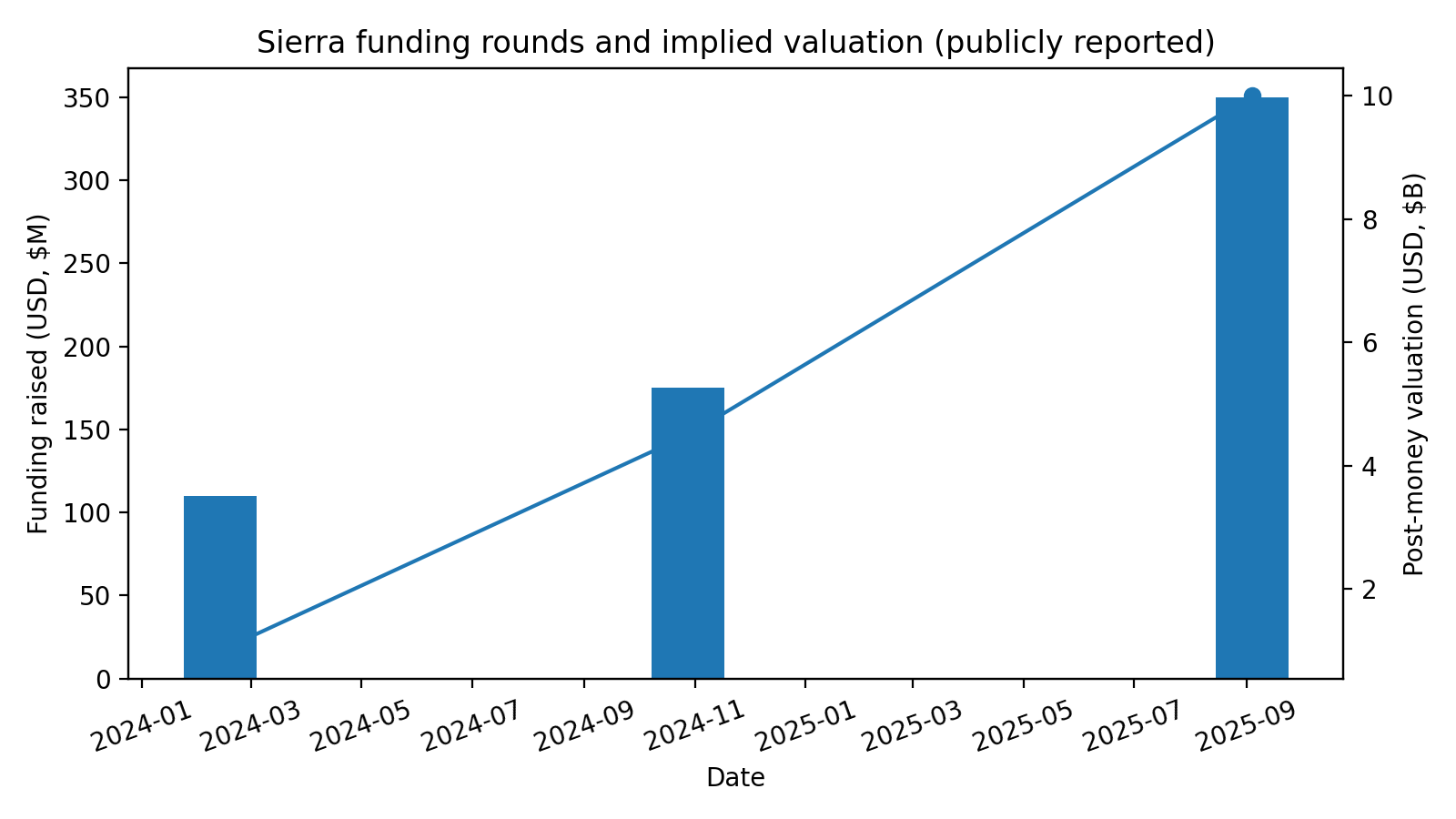

Reuters reported a $175M round led by Greenoaks and a prior $110M raise from Sequoia and Benchmark (near $1B valuation).

Sierra announced a $350M round valuing the company at $10B.

Axios reported a Softbank Vision Fund 2 investment tied to Japan expansion.

Financials

Sierra is privately held and does not publish audited financial statements. Public disclosures and official statements provide a handful of anchor points:

Late 2025: $100M ARR milestone.

Early 2026: CEO stated the company started 2026 with 150M+ ARR and referenced a ‘$50M quarter’.

Reuters reported that the company had crossed ~$20M in annualized revenue around Oct 2024.

The Default Runtime for Enterprise Customer Relationships

The optimistic endpoint is a new layer in the enterprise stack: a customer‑relationship operating system where agents handle the majority of routine interactions, humans handle the exceptions, and the system learns continuously from every conversation.

Customer service becomes proactive and personalized (because the agent remembers), not purely reactive.

Support and sales blur: the same agent that solves problems can recommend upgrades or prevent churn, if incentives and trust are managed carefully.

The ‘front door’ of the internet shifts: users increasingly start in AI interfaces (like ChatGPT) rather than on company websites; Sierra is positioning for that distribution shift.

Enterprise software absorbs agentic workflows as a first-class primitive, similar to how CRM systems became the system of record for customer interactions.