Rippling and the Employee Graph (YC W17)

The most expensive thing in your company is coordination.

Rippling is a workforce operations platform that uses a single system of record for employee data to run HR, IT, and finance workflows in one place.

The Real Problem: Coordination Costs

Customers aren’t buying payroll or device management so much as they’re buying relief from coordination costs: every hire, role change, benefit election, laptop shipment, app permission, and reimbursement becomes a tiny distributed-systems problem across teams and vendors.

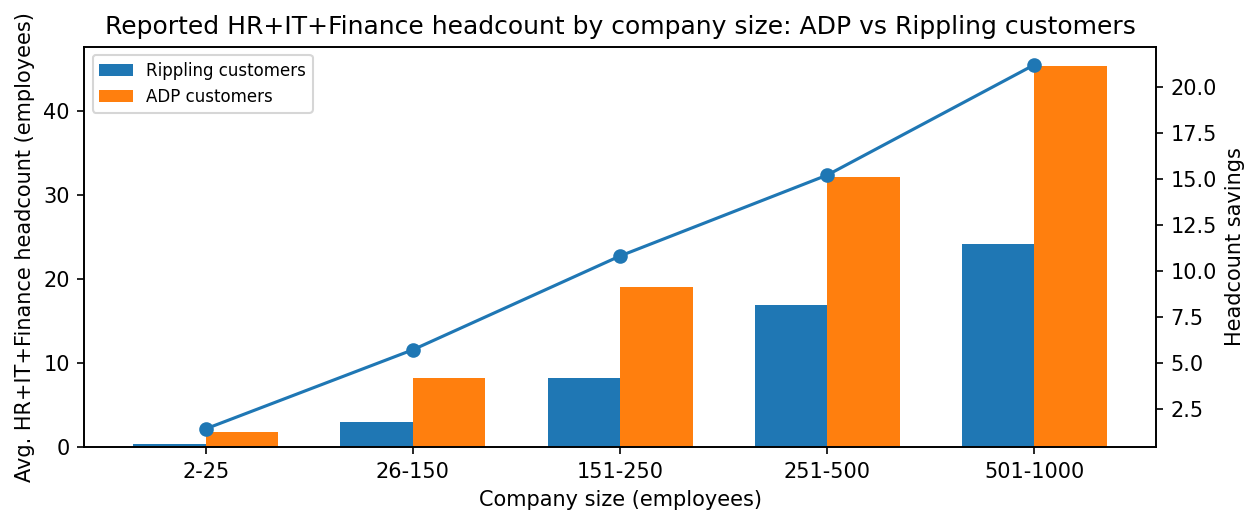

In Forrester’s TEI interviews (commissioned by Rippling), companies described legacy HRIS plus point solutions that created disjointed processes, siloed data, and no reliable single source of truth for workforce data, which then forced manual work and made it harder to scale operations.

An HRIS for employee records, a payroll processor, a benefits broker/administrator, an identity provider or SSO tool, an MDM tool for devices, an expense platform, and a patchwork of spreadsheets or admin portals that live in people’s heads. Fragmented workforce operations force HR/IT/Finance to manually coordinate changes across many systems. Errors create compliance and security risk.

One Record That Makes Workflows Compound

Most workforce software is built as separate databases with brittle integrations, while the employee lifecycle is a single causal chain. If a system can represent the organization as a graph (employees, roles, devices, apps, locations) and keep that graph high-fidelity, then automation becomes a property of the data model rather than a bolt-on.

Rippling unifies HR, IT, finance, and more on a single source of truth integrated with 500+ apps, so changes propagate rather than being re-keyed and reconciled. The unified system shows up as avoided headcount and less handoff work across teams, with quantified benefits driven by operational efficiency and consolidation of legacy tools.

If Rippling becomes the system of record for workforce identity and operations, durability comes from three compounding loops: switching costs (policies, workflows, and integrations become embedded in daily operations), data advantage (a richer employee graph enables tighter role-based controls and analytics), and distribution leverage (each added module can be sold into an installed base without re-implementing a new source of truth).

Rippling is introducing more surface area on the same data model, with new product launches such as Recruiting (an ATS built inside the platform) and on-demand custom apps built by Rippling engineers, plus IT partnerships and device-management expansions.

Rippling sits between your people data and the rest of your SaaS stack. HR enters (or imports) the canonical employee record; IT binds identity, SSO, and device inventory to that record; Finance binds payroll, expenses, and cards; and the platform layer enforces policies, permissions, and workflows across it all.

Rippling product UI example (dashboard).

Rippling’s use cases:

Onboarding/offboarding: a hire triggers provisioning (accounts, groups, SSO access), payroll setup, benefits eligibility, and device shipment; an exit triggers access revocation and device return.

Global hiring and payroll: With Employer of Record (EOR), global payroll, and contractor products as extensions of the same workforce record, which matters because global expansion is where compliance, identity, and payments collide.

IT ops for lean teams: Rippling IT emphasizes identity/access and device management as part of the same lifecycle control plane, including deeper support for Apple device fleets and management workflows.

Rippling IT example (device management overview).

The Parts Finally Clicked

Workforce operations have become both more software-defined (cloud apps everywhere) and more risk-sensitive (security, compliance, global payroll), while small-to-midsize companies still run on stitched-together systems that don’t share a reliable identity record

Historically, HRIS and payroll systems grew up as record-keeping and compliance products, not as workflow engines with open integration surfaces. IT identity and device management matured separately (often aimed at larger enterprises), while spend tools optimized around corporate cards and reimbursements. The result: each category built its own database of who works here, guaranteeing drift.

Rippling’s bet is that modern cloud infrastructure, app ecosystems, and identity standards make it practical to centralize workforce identity and push changes outward.

Payroll and HRIS began as compliance and record systems. Modern SaaS shifted them to configurable workflows, then the proliferation of SaaS apps (and remote work) made identity, device management, and permissions operationally inseparable from HR. Rippling is a product of that convergence.

Three trends matter most: SaaS sprawl (hundreds of apps per company makes manual joiner-mover-leaver processes untenable), automation expectations (workflows and approvals as table stakes), and distributed workforces (cross-border hiring and device logistics). Rippling’s product expansion into global and spend products suggests it views these as durable drivers.

Market Size: From HRIS to Workforce Ops

Rippling’s core customer appears to be small and mid-sized companies that want to run HR, payroll, IT, and spend on one platform, especially those without the appetite to stitch together a complex toolchain.

The best-fit buyer is a company whose operational complexity has outgrown spreadsheets and point tools but that still runs lean teams in HR, IT, and finance.

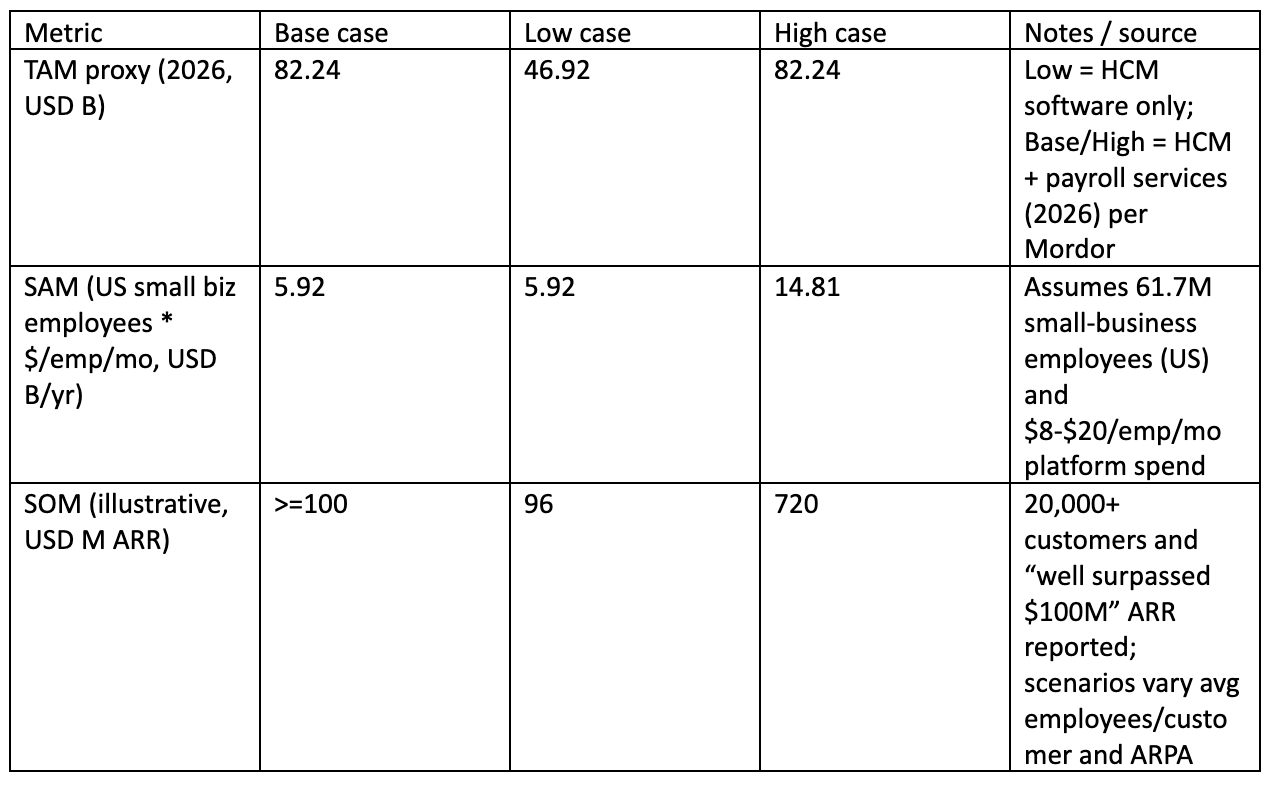

Top-down TAM: As one proxy for the HR + payroll software/services spend pool, Mordor Intelligence estimates the Human Capital Management (HCM) software market will reach $46.92B in 2026 and the global payroll services market will reach $35.32B in 2026. Summed, that is ~$82.24B in 2026. This is not a perfect TAM for Rippling (it can overlap categories and excludes adjacent IT/spend categories), but it anchors the magnitude.

Another proxy for the same broad domain is marketresearch.com, which describes a “Payroll & HR Solutions & Services” market valued at $31.0B in 2024 and projected to reach $50.4B by 2030. Different definitions produce different TAMs; in practice, Rippling’s actual economic opportunity depends on how much category boundary it can blur.

SAM/SOM are scenario-based. Rippling’s actual SAM depends on how much of the SMB/midmarket it can reach through direct sales and partners, attach rate across modules, and international footprint. None of those are fully disclosed.

Competition: Suites, Specialists, and the Status Quo

Rippling competes in a crowded valley where every vendor wants to be the system of record. The practical alternative for customers is either a legacy HR/payroll incumbent plus point tools, or a modern best-of-breed stack stitched together with integrations and human glue.

Rippling as competing with large firms such as Workday and ADP and startups such as Justworks and Deel. The surrounding adjacent set includes Paychex, Gusto, UKG, BambooHR, Okta/Microsoft Entra (identity), Jamf (Apple device management), and spend platforms like Brex and Ramp. Not all are direct equivalents: many are deep in one silo rather than broad across silos.

In practice, Rippling is often benchmarked against outsourced payroll + HRIS (ADP/Paychex + an HRIS), modern SMB stacks (Gusto/BambooHR + identity/spend), and enterprise suites (Workday/UKG) for larger midmarket.

Rippling’s plan is structural: win the employee system-of-record, then use that to collapse tool sprawl. The company argues that products built atop a rich organization graph are “better as software products” via smarter workflows, role-based policies, and analytics. Winning, therefore, is less about one feature and more about becoming the default place where changes originate.

The risk is also structural: suites can lose by being a little bit good at everything, while best-of-breed wins on depth. Rippling’s counter is to keep shipping best-in-class modules (e.g., Recruiting) while keeping the data model unified.

Advantages that could compound: a unified data model and workflow layer, breadth across HR/IT/spend enabling cross-domain automation, integration surface (apps), and customer-validated satisfaction signals.

Product: A Platform Disguised as a Suite

Rippling is a platform with multiple “clouds” (HR, Payroll, IT, Spend/Finance, Global) built on shared employee identity and data, plus platform primitives like workflows, policies, permissions, analytics, and integrations.

Form factor: cloud software accessed via web and mobile, sold as modular products. The platform layer advertises core capabilities including Workflow Studio, Analytics, Policies, Permissions, Integrations, and App Studio.

Functionality spans HRIS and talent (e.g., recruiting, performance, learning), payroll (including global), IT identity and device management, and spend products such as expense management and corporate cards.

Architecture: one single source of truth for employee data with integrations out to third-party apps. A unified workforce data layer enabling workflow automation, analytics, and permissions.

Roadmap signals include: building more best-in-class modules on top of the employee graph (Recruiting), expanding the platform’s ability to support bespoke workflows (Rippling Solutions: custom apps built by Rippling engineers), and deepening IT operations coverage (including Apple device fleet management).

Business Model: Land the Record, Expand the Workflows

Rippling’s business model is SaaS subscription sold in modules, typically priced per employee per month, with additional monetization through adjacent services (payroll processing, PEO/EOR, benefits) where take-rate and cost structure can differ from pure software.

The platform math: acquire customers via a compelling wedge (often payroll/HRIS or IT identity/device), land with a core record, then expand with adjacent modules that increase ARPA and raise switching costs.

Public pricing disclosures are limited. Rippling’s small-business page states a platform fee starting at $8 per user per month plus a $40 per month base fee, with products sold modularly. The broader pricing page emphasizes customized pricing via demos (not a public rate card).

Incentive-wise, per-employee pricing aligns Rippling with customer growth (a good incentive when churn is low) but also makes the product feel like a tax during downturns. The durability test is whether Rippling can continue to justify module expansion through measurable labor savings, consolidation of vendors, and risk reduction.

Rippling reported serving over 20,000 customers and having well surpassed $100 million in annual recurring revenue (ARR) as of May 2025. Those imply a minimum average ARR per customer of >$5,000 (i.e., $100M / 20k) but do not reveal distribution, cohort retention, or payback.

Sales and distribution model is not fully disclosed. Rippling highlights partner channels (brokers, accountants, VC firms/accelerators, tech partners) alongside direct demo-led sales. The mix likely varies by segment: SMB may be more self-serve or partner-driven; midmarket may be more direct sales.

Team: Operators Building Operators’ Software

Founded in 2016 by Parker Conrad and Prasanna Sankar, Rippling’s team story is a founder-led, product-heavy company trying to win a systems category by out-building incumbents: heavy R&D emphasis, rapid product expansion, and a thesis-driven CEO narrative centered on data integrity and automation. The company’s leadership team includes Matt MacInnis (COO), Albert Strasheim (CTO), Adam Swiecicki (CFO), and Matt Plank (CRO).

Rippling had 2,800 employees and more than $1 billion in cash as of April 2024, and expanding globally with offices across the U.S., India, Ireland, the UK and Australia.

Financials: What We Know, What We Infer

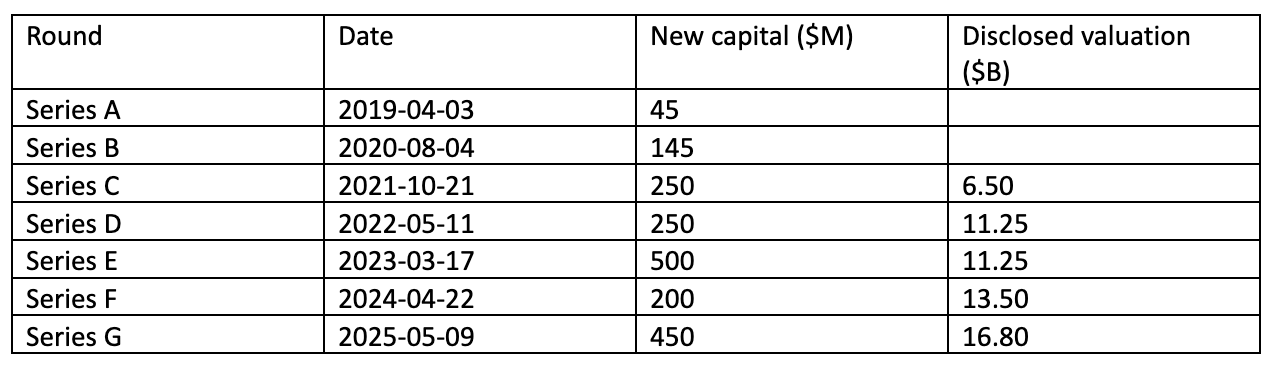

In March 2023, during the SVB collapse, Rippling used $130 million from its balance sheet to ensure payrolls were processed and raised $500 million in a Series E round at the same valuation as its 2022 Series D ($11.25B), a vivid example of liquidity as a product requirement in payroll. Rippling had over $1 billion in cash as of April 2024. As of May 2025, Rippling surpassed $100 million in annual recurring revenue (ARR) and served over 20,000 customers.

The company has arranged secondary liquidity via tender offers, Series F tender up to $590M, and Series G repurchase up to $200M, which signals both investor demand and employee liquidity needs.

Because Rippling is private and does not publish audited financials, any P&L-style model is necessarily assumption-driven. Two high-level inferences are reasonable, with uncertainty:

Software vs services mix: A larger share of payroll/PEO/EOR and payments-like products could lower gross margin and increase compliance/operational costs relative to pure HRIS SaaS (directional inference, not measured here).

Operating leverage: If Rippling’s platform genuinely reduces customer ops headcount, its own sales efficiency and support costs will determine whether those savings translate into pricing power and durable owner-earnings.

A more defensible economics datapoint is the TEI report’s framework: it provides a composite-org model with ROI 136% and payback <6 months.

Vision: The System Companies Run On

If Rippling executes, it will become the default workforce operating system for the SMB and midmarket: the place where identity, payroll, access, devices, and spend rules are defined once and enforced everywhere.

In five years, the most plausible win is that Rippling the authoritative graph of an organization for a large cohort of companies. That would mean: most workforce-triggered actions (joiner/mover/leaver, expense eligibility, app access) originate from Rippling, third-party tools treat Rippling as the upstream identity provider, and analytics and policy enforcement become differentiators.

There are multiple plausible trajectories. A few high-level scenarios:

Platform winner (higher probability if data model stays clean): Rippling expands modules but keeps one coherent admin experience; attach rates rise; the platform becomes sticky infrastructure.

Enterprise squeeze (risk case): incumbents defend midmarket with bundling and distribution; Rippling succeeds but remains primarily SMB, capping ASP and slowing owner-earnings growth.