Factory Is the Weapon

Inside Anduril’s attempt to turn software and production scale into military advantage.

Anduril is building a defense company organized around autonomy software, integrated hardware, and production scale. Lattice and mission autonomy on the software side, a widening menu of products on the hardware side, and a wager that manufacturing capacity is itself strategic terrain. It is trying to replace parts of the legacy prime-contractor model with a software-defined, manufacturing-aware one.

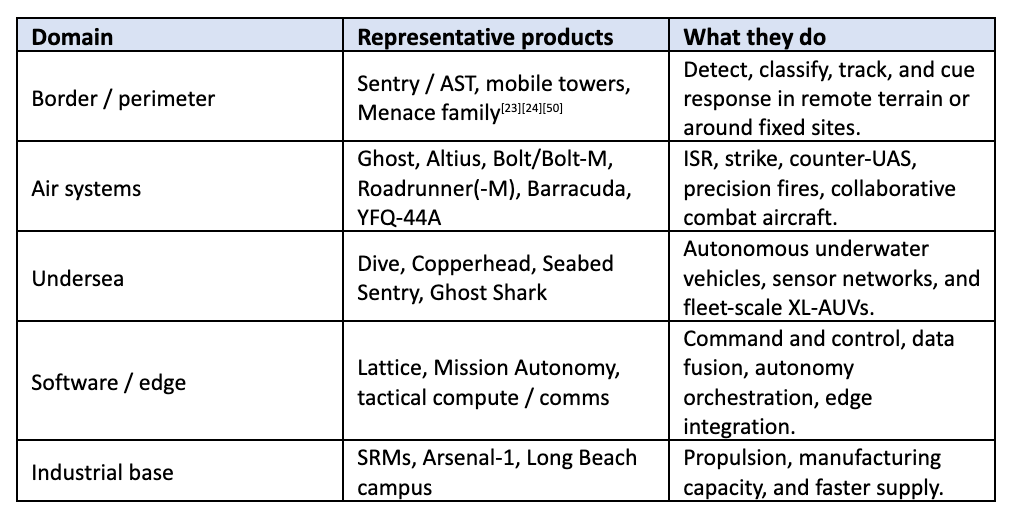

Its footprint now spans border surveillance towers, counter-UAS systems, autonomous aircraft, loitering munitions, undersea vehicles and sensors, mixed-reality soldier systems, space-surveillance command modernization, and solid rocket motor production.

The Problem Anduril Is Actually Solving

The current system buys too slowly, too expensively, and too bespoke for an era defined by cheap sensors, autonomy, and rapid iteration. Militaries and border-security agencies need persistent awareness, faster decision cycles, and more output per operator than legacy procurement and legacy architectures reliably provide.

Today that pain is addressed through a patchwork of manual surveillance, stovepiped sensors, man-in-the-loop piloting, large exquisite platforms, and cost-plus development programs that reward time and complexity as much as results. Under cost-plus contracts, expense, delay, and engineering sprawl can be economically rational for the contractor even when they are strategically irrational for the buyer.

On the operational side, the military problem is one of scale. The core warfighting function is still find, engage, assess. The bottleneck is that sensor counts and data volumes are exploding while humans cannot manually absorb or act on all of it. On the industrial side, supply chains are brittle. Anduril’s move into solid rocket motors addresses a chokepoint. Until Anduril’s entry, the United States had only two suppliers of this category, and the industrial base has become too concentrated to deliver speed and volume in a serious contingency.

Border Patrol hires towers and software to detect, classify, and track activity in remote terrain without stationing people everywhere. A base-defense customer hires a counter-UAS stack to convert a swarm threat from a manpower drain into a software-supported intercept problem. An air arm hires a collaborative aircraft or an attritable cruise-missile family to add mass without paying exquisite-platform economics. In each case, the job is progress under operator, time, and cost constraints.

A defense market designed to maximize cycle time, minimize competitive entry, and protect incumbent economics is almost a machine for under-delivering autonomy. That does not guarantee Anduril wins. But it does explain why a serious entrant could emerge at all.

Software First, Hardware Second, Factory From Day One

Anduril treats modern defense as a software problem first, a hardware problem second, and a production problem from the beginning. It promises the customer not one more isolated widget, but an integrated stack that sees more, decides faster, and fields capability sooner.

Lattice is Anduril’s open software platform for public safety, security, and defense, while Mission Autonomy is the layer that enables teams of unmanned systems to collaborate across land, sea, and air. Around that software core sit products that are physically very different but operationally related. Sentry and mobile towers for remote surveillance. Ghost and Altius for airborne sensing and strike. Roadrunner for reusable vertical-launch interception. Barracuda for hyper-scale, attritable air vehicles. Bolt-M for Organic Precision Fires-Light. YFQ-44A for collaborative combat aircraft. Dive, Copperhead, and Seabed Sentry for undersea missions. And EagleEye for soldier-worn mission command at the edge.

It changes the labor equation and the time equation. Border security becomes persistent remote monitoring with autonomous cueing instead of constant physical presence. Air defense becomes an operator-supervised, reusable interception problem rather than an always-manual hunt. Undersea awareness becomes a mobile sensor-network problem rather than only a crewed-platform problem. And airpower gains a path toward affordable mass instead of buying only a few exquisite aircraft that cannot be risked casually.

The durable part is the fit across activities. Software reuse, rapid prototyping, common autonomy logic, manufacturing investments, and selective acquisitions at bottlenecks. That fit is visible in the way the product family keeps widening while still pointing back to open architecture, operator supervision, autonomy at the edge, and manufacturability.

The company is expanding tactical compute and communications through Klas, radar and command-and-control through Numerica, infrared sensing through AIRS, and mixed reality through Microsoft, Meta, and EagleEye. The direction of travel is toward tighter coupling between what the operator sees, what the machine infers, and what effectors can be tasked in response.

Why This Could Only Happen Now

Three curves have crossed. Autonomy software is good enough to matter, commercial components and supply chains are rich enough to exploit, and the strategic environment now rewards affordable mass rather than only exquisite scarcity. The old model aged into a target at exactly the moment the new technical stack became practical.

Historically, the U.S. defense system could tolerate long cycles because it was buying technological superiority in relatively concentrated chunks. That bargain has weakened. Post-Cold War consolidation left the industrial base hyper-concentrated in a handful of firms, the resulting technology base became slow and lethargic. Anduril’s founding in 2017 was a direct response to that opening. A bet that Silicon Valley methods, commercial supply chains, and mission urgency had finally become compatible with national-security demand.

In 2017 computer vision was just beginning to work reliably enough, and Anduril was adapting desktop GPUs to operate in hot desert conditions under solar power. On the commercial side, the only way out of the munitions and autonomy volume problem is to design around commercial and industrial supply chains rather than around bespoke defense-only parts.

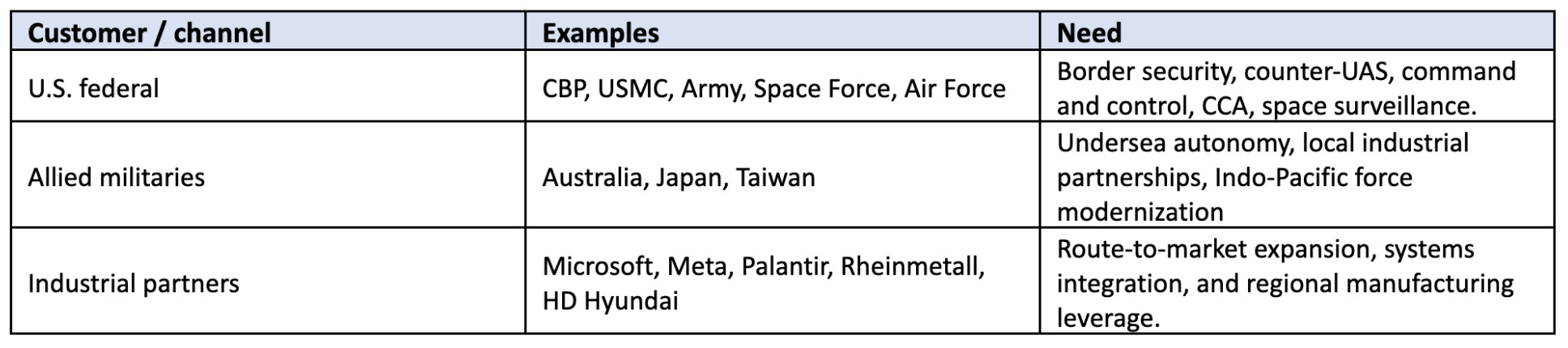

Since 2024 the company has accumulated a set of validations that would have been hard to imagine for a defense-tech startup a decade earlier. A Space Force program of record, a $200 million Marine Corps MADIS award, a $99.6 million Army NGC2 prototype award, a $159 million mixed-reality award, an Air Force CCA designation and flight testing track, an Australian program-of-record XL-AUV award, and an expanding allied footprint spanning Europe and the Indo-Pacific.

This also required a financing regime willing to tolerate aggressive upfront spending before the full revenue base existed. Anduril’s funding path, from Series D in 2021 to a $30.5 billion valuation in 2025, with an additional March 2026 raise shows that private capital now believes there is room for a category-defining defense company that stays private long enough to build real industrial muscle.

How Big the Prize Really Is

Anduril’s market is large enough to matter even on a conservative U.S.-only lens. Its categories overlap procurement, R&D, border security, autonomy software, and industrial-capacity spending.

In the United States, U.S. Customs and Border Protection, the Marine Corps, the Army, the Space Force, and the Air Force. Abroad, Australia is already a fleet-scale undersea customer, Japan and Taiwan have become formal expansion geographies, and Rheinmetall and HD Hyundai show how Anduril is also positioning as a supplier and co-manufacturer inside allied industrial ecosystems.

The President’s FY2025 DoD budget request was $849.8 billion. For a conservative core-TAM lens, we use only the U.S. DoD top line and assume that between 2% and 4% of that pool is realistically addressable by the mix of autonomy, command-and-control, border-adjacent national-security systems, attritable aircraft and munitions, undersea autonomy, and related industrial-capacity programs where Anduril is competing. That yields a U.S.-core annual TAM range of roughly $17.0 billion to $34.0 billion, with a base case of $25.5 billion at 3%. This excludes allied budgets, which are themselves rising materially in Australia, the UK, Japan, and Taiwan.

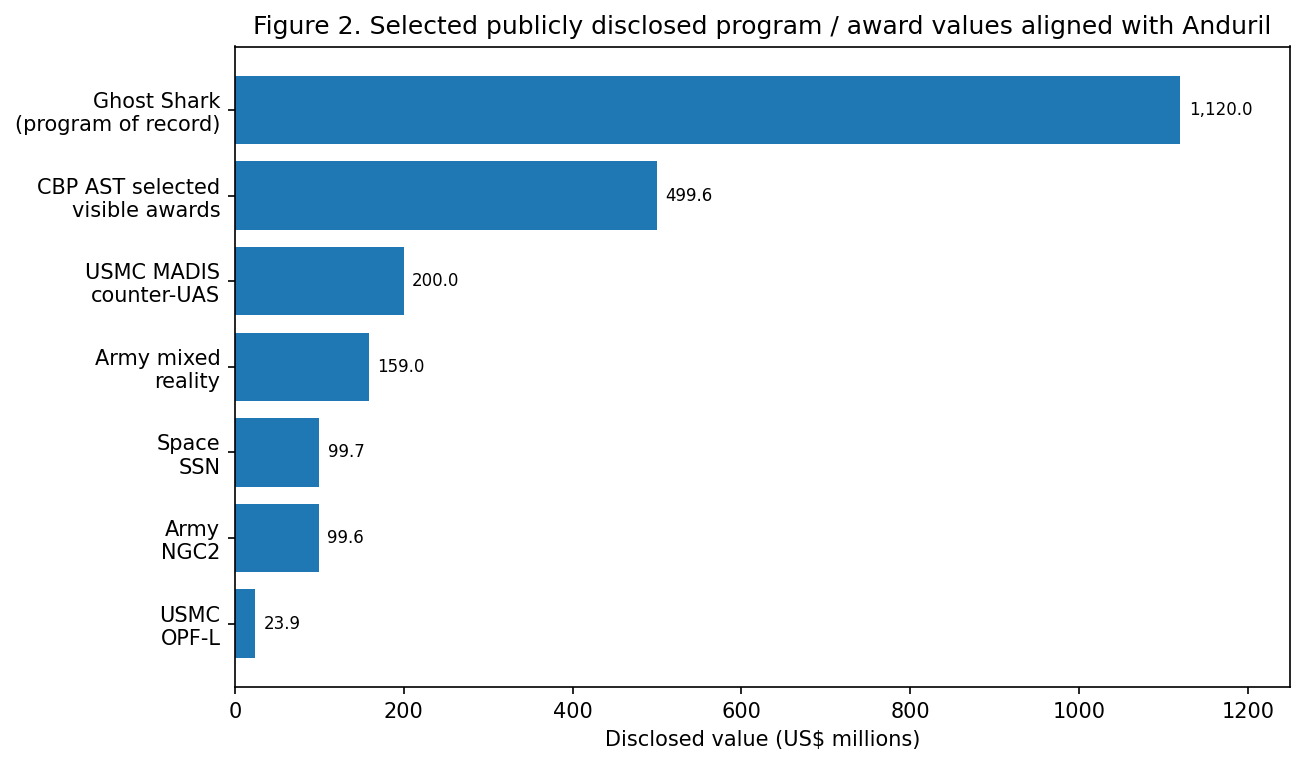

Using selected publicly disclosed award or program values, CBP AST task orders, MADIS, NGC2, the Space Surveillance Network modernization effort, the mixed-reality award, OPF-L, and Ghost Shark, the visible floor already exceeds $2.2 billion.

TechCrunch reported that Anduril doubled 2024 revenue to about $1 billion. Anduril appears to have crossed into real operating scale while much of its manufacturing buildout is still ahead of it.

The Real Rival Is the Old Defense Model

Anduril’s competition are two systems. First, the legacy prime-contractor stack, optimized for bespoke cost-plus programs and exquisite platforms. Second, the newer point-solution startup stack, optimized for one niche but often missing the software, manufacturing, or procurement breadth to become a durable prime-scale business.

The direct competitive set changes by mission. In collaborative combat aircraft, General Atomics is the most obvious peer because the Air Force designated both the YFQ-42A and Anduril’s YFQ-44A inside the same program. In border surveillance, the alternatives include existing tower and video-surveillance architectures, fixed-site legacy systems, and manpower-heavy approaches. In counter-UAS and air defense, Anduril is competing against both incumbent air-defense vendors and narrower counter-drone offerings. In undersea autonomy, the alternatives include naval primes and specialized robotics firms. The company is entering many adjacencies where the common denominator is autonomy plus integration.

The plan to win is to be unique in the structure of the activity system. Anduril combines a shared software and data layer, hardware families designed around manufacturability, strategic acquisitions at bottlenecks, and selective partnerships that widen distribution or capability without forcing the company to invent everything itself. Microsoft and Meta matter in mixed reality. Palantir matters in some command-and-control and intelligence contexts. Rheinmetall and HD Hyundai matter for regional industrial leverage.

Incentives matter. If cost-plus incentives reward slowness and complexity, Anduril’s opportunity is to behave more like a product company, fund ahead of contract, integrate fast, field early, and then scale. The risk is that the system drags Anduril backward into prime-like behavior as programs get larger. The company’s moves into propulsion, compute, radar, and factory buildouts suggest management understands that competition is partly about who owns the chokepoints.

Competitive advantages, stated plainly.

a reusable software and autonomy stack

cross-domain product reuse rather than one-off systems

increasing control over supply and production bottlenecks

a willingness to partner rather than enforce total vertical purity

evidence of real adoption in programs that matter

From Towers to CCAs to Undersea Drones

The product is a family of interoperable systems tied together by software. Anduril keeps expressing the same design priorities. Autonomy operator supervision, modularity, open integration, and manufacturability, across very different form factors.

On land, the company’s counter-intrusion and base-security products start with sensing and perception. Radar-cued towers, cameras, edge software, and mission command. In the air, it has built a ladder from tactical aircraft like Ghost and Altius to reusable jet-powered interceptors like Roadrunner, to precision-fires systems like Bolt-M, and then to Barracuda and YFQ-44A at the larger attritable/CCA end of the spectrum. At sea and undersea, the portfolio now includes Dive-derived vehicles, Copperhead, Seabed Sentry, and Ghost Shark. At the operator edge, EagleEye and the Meta/Microsoft-linked mixed-reality work pull command and AI directly onto the warfighter.

YFQ-44A was designated by the Air Force in March 2025, began flight testing in October 2025, and by February 2026 had entered deliberate weapons-integration/captive-carry testing. Barracuda-500 moved forward in the Enterprise Test Vehicle project after a September 2024 flight test, while Barracuda-100M posted another successful flight test in July 2025. Ghost Shark went from prototype to program of record and opened a Sydney factory ahead of schedule. Those milestones are not the whole roadmap, but they are enough to say the company is moving from prototype theater into the harder world of repeatable build-test-scale loops.

Anduril’s acquisitions make most sense when viewed as capability splices into that architecture. Altius from Area-I, undersea capability from Dive, propulsion from Adranos, Group 5 aircraft from Blue Force, radar and C2 from Numerica, tactical compute from Klas, and infrared payloads from AIRS.

Can Defense Work Like a Product Business?

Anduril is trying to make defense money like a product company rather than like a classic cost-plus contractor. The model is to develop capability ahead of demand where necessary, sell integrated systems and software into government programs, add sustainment and support, and increasingly capture industrial economics by owning more of the manufacturing and subsystem stack.

The company has significant program activity in border surveillance, counter-UAS, C2, mixed reality, space surveillance, uncrewed aircraft, and undersea systems. It has also built partnership channels rather than insisting on doctrinal purity. Microsoft for IVAS, Meta for XR hardware and software acceleration, Palantir for TITAN and edge hardware interoperability, Rheinmetall for European production, and HD Hyundai for naval scale. That mix looks like a hybrid of prime, subsystem provider, and software platform owner.

The sales and distribution model have four channels. First, direct sales and program wins with U.S. agencies. Second, allied direct sales and local industrial relationships. Third, partner-enabled bids where Anduril contributes hardware, software, or manufacturing into a broader program. Fourth, emerging component/supplier economics in categories like solid rocket motors, where the customer may be another defense contractor rather than the end government buyer.

It has raised large private rounds, but it has not spent them on random adjacency hunting. Instead, acquisitions line up with chokepoints. Payloads, motors, compute, radar, undersea, larger autonomous aircraft. Arsenal-1, the Mississippi motor line, the California expansion, and the Sydney factory all reinforce the same message. Anduril wants the economics of product plus throughput, not the economics of bespoke integration alone.

The Founder Group Behind the Bet

The key team story is one of a coherent operating group. Anduril’s founder set gives the company a shared worldview about software, deployment speed, and institutional friction, but with enough role differentiation to avoid becoming a one-man show.

Palmer Luckey supplies the founding ambition and the public polemic. Schimpf appears to be the systems builder and operating explainer, repeatedly returning to the same themes. Software leverage, autonomy at scale, and procurement incentives. Stephens bridges venture logic, government relationships, and the capital-allocation mindset. Grimm, as COO, is central to the company’s manufacturing and scale story. Chen is the least publicly visible of the founding group but is part of the official leadership bench. Brose adds a different layer altogether. He is less a startup operator by origin than a translator of strategy, military need, and bureaucratic reality, and his January 2025 promotion to president signals that Anduril sees that translation layer as core.

They have raised capital aggressively, but also placed a series of early and expensive bets on manufacturing footprint, propulsion, radar, tactical compute, and undersea capability. That is not how a typical venture-backed hardware startup behaves unless management believes it is building a lasting institution/

The Palantir adjacency is important. It is evidence that parts of the team had already spent years learning how to sell difficult software into hard government problems. At the same time, Luckey’s consumer-tech and hardware pedigree expands the ambition beyond enterprise software. The resulting blend, software-governed, hardware-serious, politically literate, and culturally combative, helps explain why the company can be both product-heavy and narrative-heavy without collapsing into pure theater.

The Financial Fog, and the Signals That Matter

Statement-level financial disclosure is minimal because Anduril is private. Funding history and valuation history show that capital markets have repeatedly re-underwritten the story. The best hard evidence today is operational. Programs, factories, tests, and customer expansion.

The New Prime Question

If all goes well, five years from now Anduril will have built a credible alternative template for how Western defense capability gets designed, produced, and fielded. The optimistic case is that it becomes too real, too useful, and too scaled to be treated as an outsider anymore.

In the bullish version of 2031, Arsenal-1 is hot, the Mississippi motor line is mature, the California expansion is fully utilized, and the Sydney factory is a template. YFQ-44A or its descendants are in service or on a clear service path. Barracuda is a real attritable mass weapon. Ghost Shark is a fleet. Mixed reality, body-worn mission systems, and edge autonomy have tightened the loop between sensing, command, and effect. Lattice has become a military operating layer into which partners plug. In that world, Anduril would look like a new prime built around a different set of assumptions.

The prize is durable owner economics from a business that can keep reinvesting at high rates because its products, software, and production assets reinforce one another. The moat would be continuity of positioning, staying committed to affordable mass, software-defined systems, and manufacturing speed even as scale and bureaucracy tempt imitation of the legacy model.

The bear case, Anduril could become just another systems integrator. Programs could slow as they enter the swamp of record procurement. Manufacturing could prove harder than management expects. Allies could like the brand more than they buy the products. Or the company could simply become so broad that it loses the discipline that made it dangerous in the first place.

If you frame the next five years as a distribution, the left tail is a well-funded but ordinary defense contractor. The middle case is a very successful prime-adjacent company with strong niches in autonomy, sensing, and selected weapons. The right tail is a true new-prime outcome. A company that changes how the West thinks about industrial capacity, autonomy, and procurement. The reason investors care is that the right tail is genuinely large. The reason analysts should stay humble is that the path runs through manufacturing, programs of record, and warfighting relevance.